What is an EMI scheme? EMI share options explained

An EMI scheme is by far the most generous mechanism with which to award employees with equity in your company. Here's wh...

Already have an account? Log in

Create and manage your EMI scheme on our automated platform with unlimited help from our EMI experts.

companies use SeedLegals

EMI schemes in the UK are set up on SeedLegals

lower price than lawyers and accountants

EMI share options are a low cost, tax efficient way to reward your UK staff with equity.

Join over 14,000 UK companies using EMI schemes.

Attract, retain and motivate staff Align your team with your company goalsGet Corporation Tax relief for your company Grant tax-advantaged options to your staff

Attract, retain and motivate staff Align your team with your company goalsGet Corporation Tax relief for your company Grant tax-advantaged options to your staff

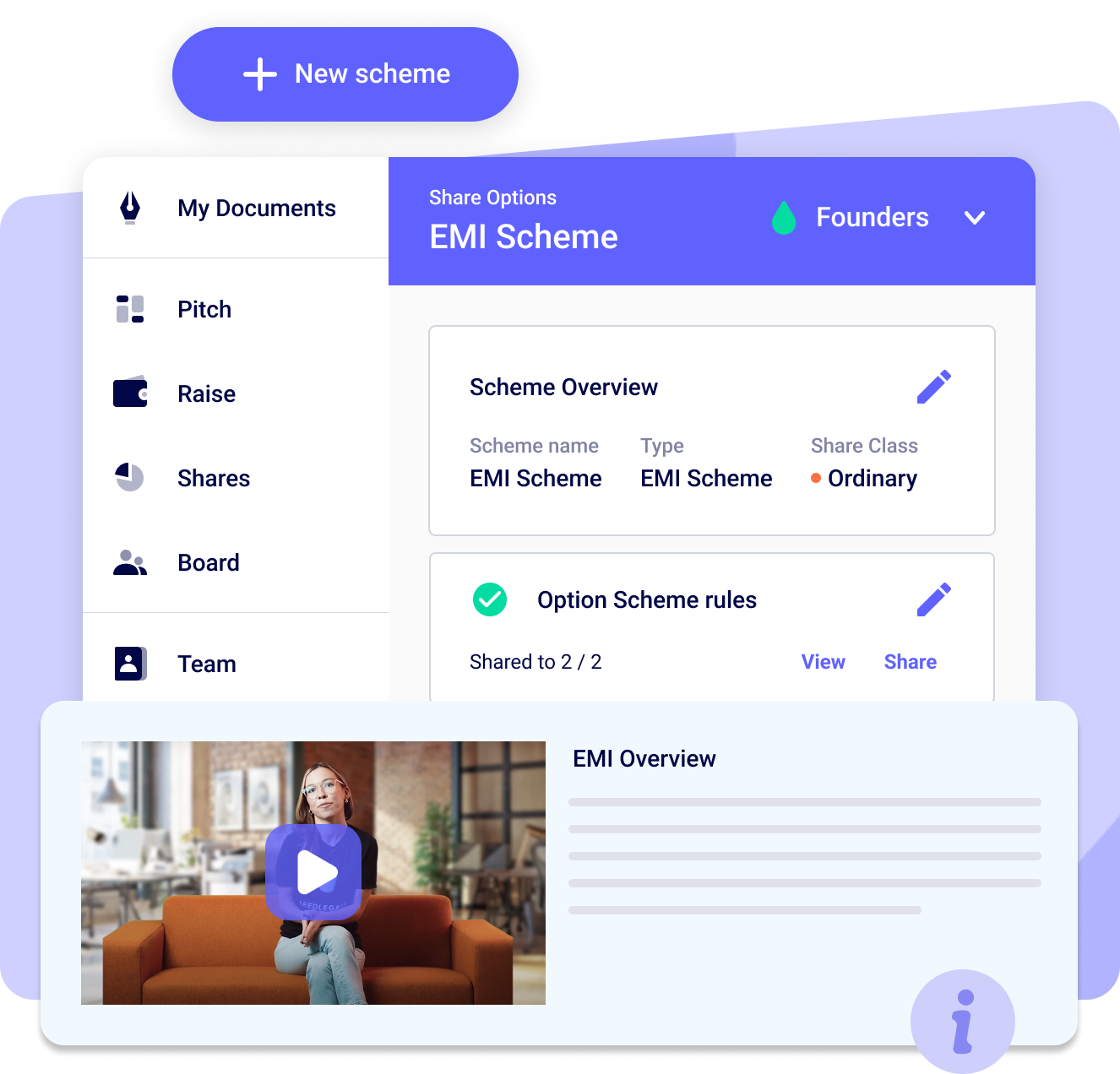

Generate all the documents automatically. Our EMI experts check the details for you and they're on hand if you need any help.

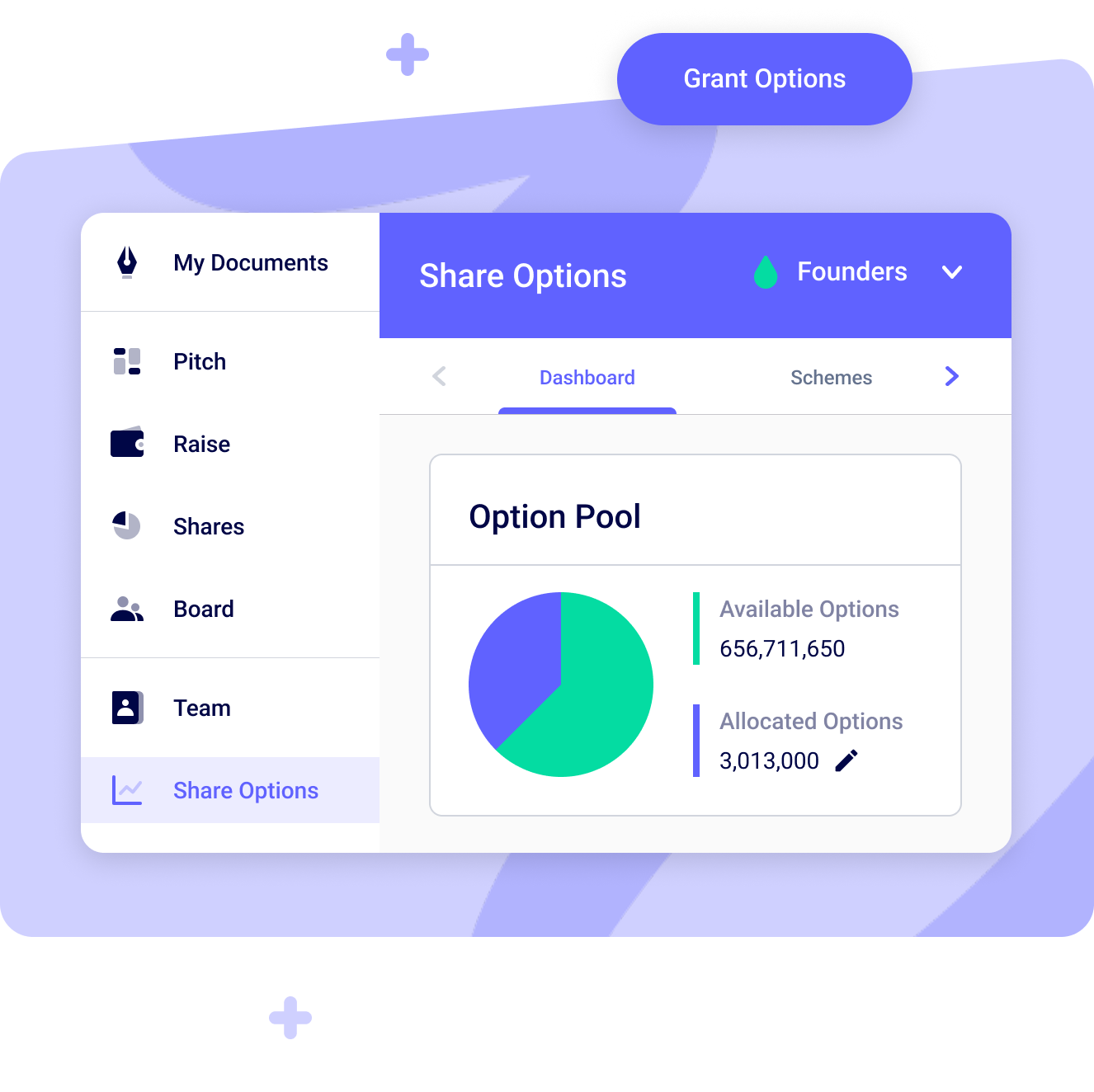

Build and customise your scheme Sign and store all the documents on SeedLegals Add new joiners anytime, issue option grants instantlyView options issued and exercised

With our easy-to-use option holder portal, employees can watch the worth of their options grow and track vesting.

Employee portal included in your membership Keep employees motivated and engaged For options holders: track vestingFor options holders: use the calculator to see what options would be worth for any valuation

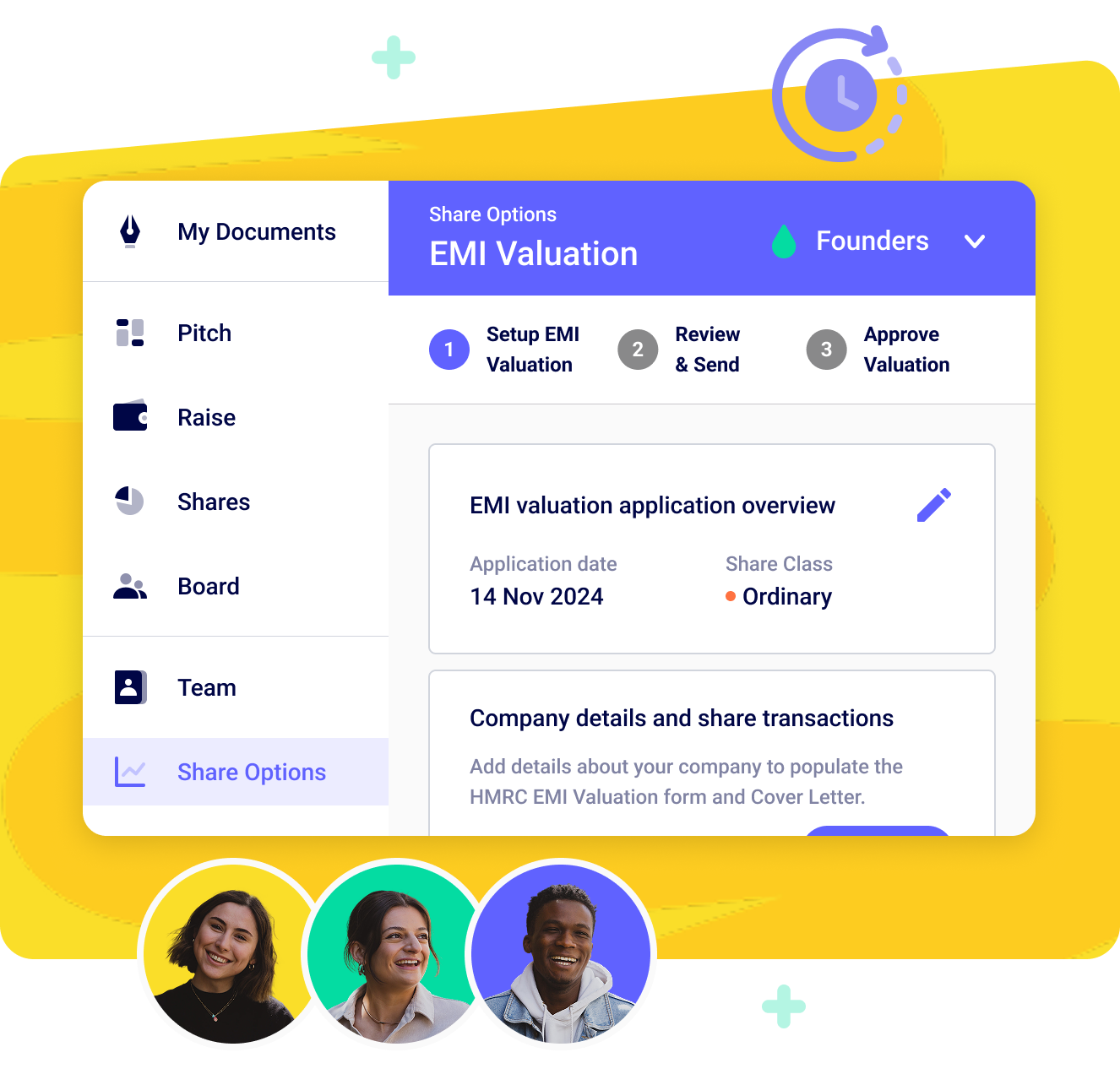

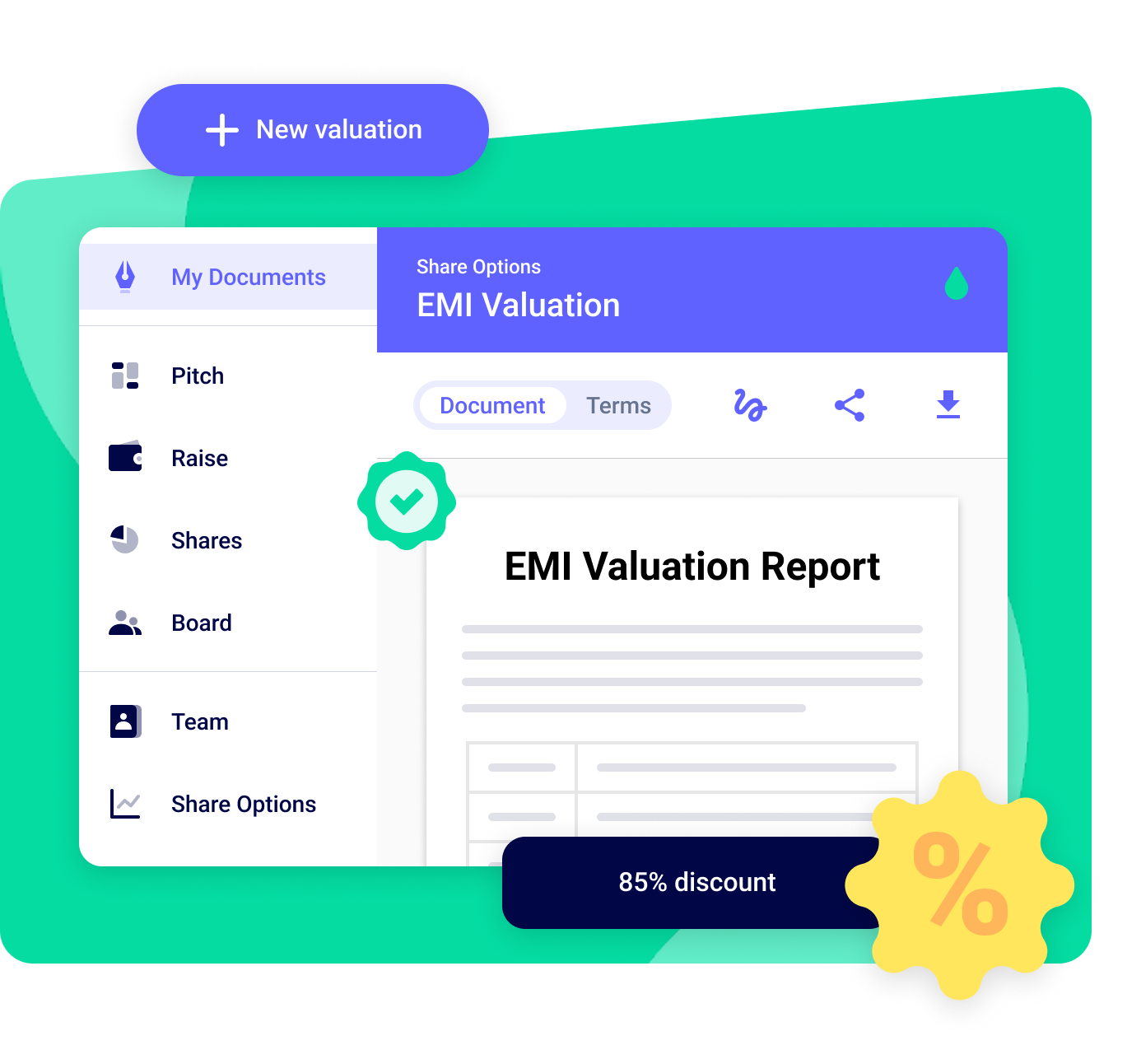

Our valuation tool builds your EMI valuation report in minutes to help you achieve the best possible discount for your employees - up to 70%.

Get an accurate EMI valuation for your company and employeesTrust our proven, HMRC-compliant processSpeed up your EMI valuation and get approved fast

Our team of EMI experts is on hand to guide you where needed, answer your questions and review your documents.

Unlimited support is included at no extra costTalk to us via chat, phone, email or video callAsk us anything - we're here 9am to 6pm Monday to Friday

Frequently asked questions about EMI share option schemes

What is an EMI share option scheme?

How do I set up an EMI scheme?

What do SeedLegals EMI experts help with?

What are the tax benefits of EMI options for my business?

What are the tax benefits of EMI options for employees?

What are the qualifying conditions for an EMI scheme for companies?

What are the qualifying conditions for an EMI scheme for employees?

How much does it cost to set up an EMI scheme?

What is the share options calculator and how does it work?

What are the most important dates for the EMI Option Scheme

What is an EMI Valuation and why do I need one?

How to setup your EMI options scheme on SeedLegals

Why do I want a low EMI Valuation?

What are the most common mistakes on the EMI valuation

An EMI scheme is by far the most generous mechanism with which to award employees with equity in your company. Here's wh...

Find out how startups structure their option schemes in this report by our experts. Read insights and analysis based on ...

A detailed guide to EMI Share option scheme qualifying criteria for companies and employees, plus other ways to give sha...

Our team of legal and funding experts have helped thousands of entrepreneurs raise money and grow their businesses.

Your company's core agreements, all in one place

Share and collect signatures online via SeedLegals

Create the exact documents you need at every stage of growth

Your information stays safe and confidential in our secure system

Talk to one of our friendly team anytime on live chat

Don't worry, our insurance covers claims related to our platform

From food to FinTech and beyond, join thousands of startups who use SeedLegals to start, raise and grow faster.

More customer stories

The reality is you’re on a journey; fundraising is so much about the narrative. SeedLegals allows you to tell the right story at the right time with the right legal documents for different types of investors.

Founder & CEO, Yoller

SeedLegals held our hand through complex investor negotiations and even picked up on some errors produced by our previous lawyers which were a well-known City law firm!

Founder & CEO, Qured

One of the great things about SeedLegals is that it is designed to be appropriate for the round and the stage of the business. They keep it simple. It feels like they really understand that.

Co-founder & CEO, Pluto

How do I get all the businesses I invest in to use SeedLegals?

Angel Investor , The Family

It's easy to forget about the legal side of things but SeedLegals make things really easy to understand. The team at SeedLegals are truly amazing.

Founder, TRIM-IT

There’s an opportunity to reach a specialist advisor via chat, phone and email to check in on anything. The SeedLegals team were extremely responsive – really amazing.

Co-Founder, OddBox