How to use Instant Investment to raise money before the end of the tax year

Some prospective investors hurry to invest in January, February or March. We explain why the tax year end creates an inv...

Already have an account? Log in

Use Instant Investment to top up a previous round and add new investors anytime.

No need to wait until you do a funding round - add investments whenever you need to.

More freedom - fundraise your wayMore flexibility - seize opportunities as they ariseMore time - stay focused on growing your business

More freedom - fundraise your wayMore flexibility - seize opportunities as they ariseMore time - stay focused on growing your business

Not sure how it works? Wondering how much equity to give away? We've helped thousands of companies fundraise - talk to our experts to get answers, fast.

Talk to us via live chat, phone, email or video call Unlimited help included for members - no billable hoursAsk us anything - we're here 9am to 6pm Monday to Friday

Some prospective investors hurry to invest in January, February or March. We explain why the tax year end creates an inv...

New data shows the way that startups are raising investment is changing, and SeedLegals is pioneering that change.

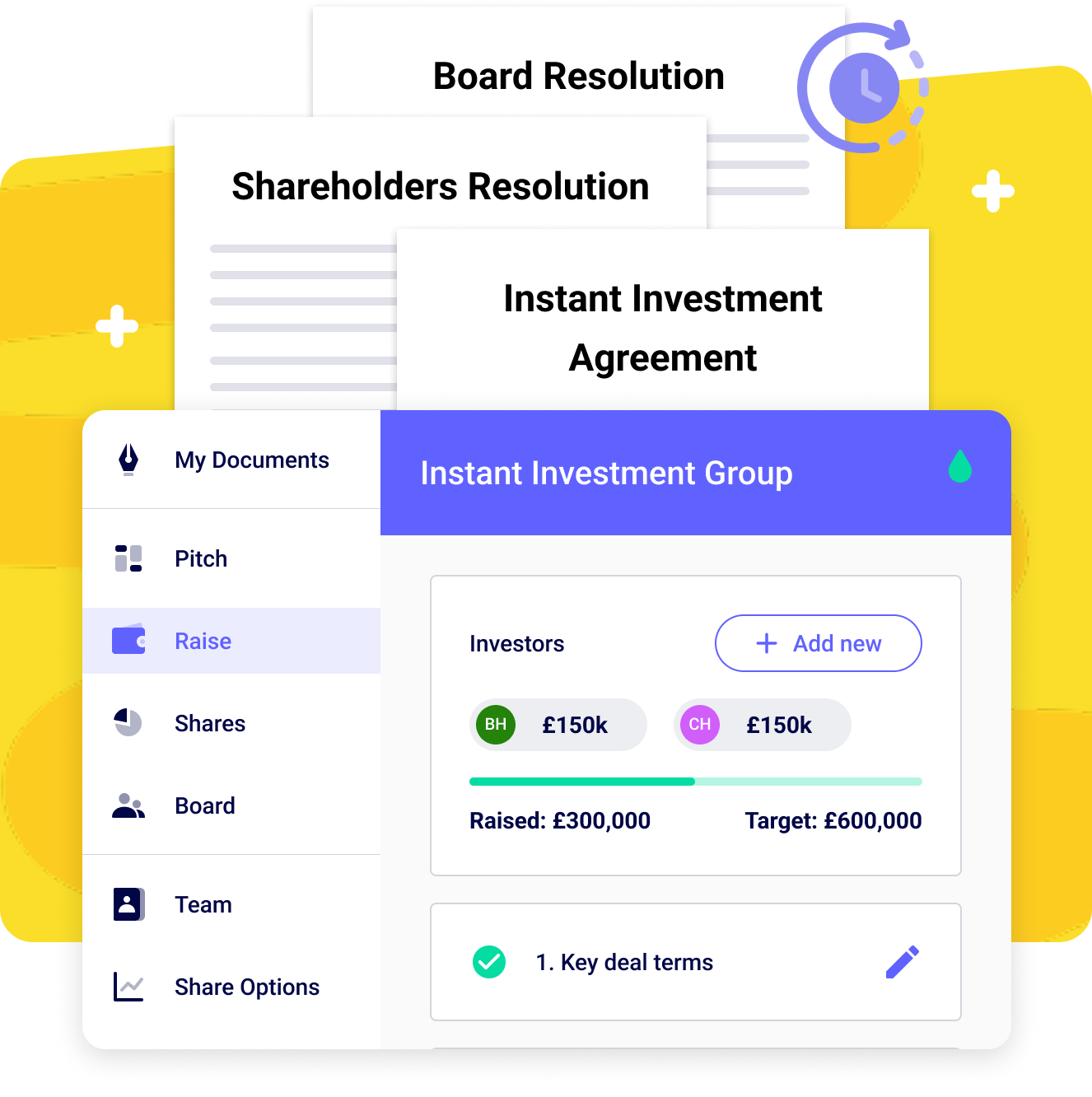

Why wait until your next funding round? Accept new investment to your startup in minutes at any time with SeedLegals Ins...

How much can I raise with Instant Investment?

Can I use Instant Investment if I haven’t done a funding round on SeedLegals before?

How do I do an Instant Investment?

What documents do I need for an Instant Investment?

Should I do a SeedNOTE/SeedFAST or an Instant Investment?

How many investments can I receive with Instant Investment?

What does a ‘rolling close’ mean?

What is agile funding?

I still have questions about Instant Investment…

Our team of legal and funding experts have helped thousands of entrepreneurs raise money and grow their businesses.

Your company's core agreements, all in one place

Share and collect signatures online via SeedLegals

Create the exact documents you need at every stage of growth

Your information stays safe and confidential in our secure system

Talk to one of our friendly team anytime on live chat

Don't worry, our insurance covers claims related to our platform

From food to FinTech and beyond, join thousands of startups who use SeedLegals to start, raise and grow faster.

More customer stories

The reality is you’re on a journey; fundraising is so much about the narrative. SeedLegals allows you to tell the right story at the right time with the right legal documents for different types of investors.

Founder & CEO, Yoller

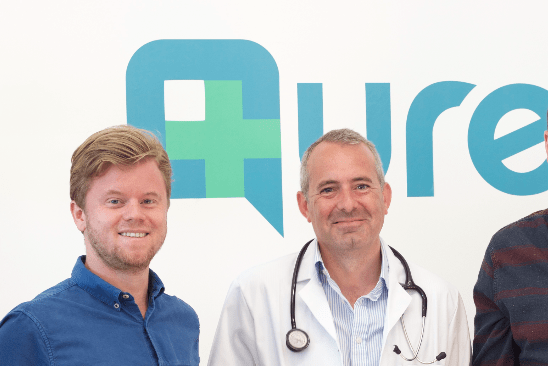

SeedLegals held our hand through complex investor negotiations and even picked up on some errors produced by our previous lawyers which were a well-known City law firm!

Founder & CEO, Qured

One of the great things about SeedLegals is that it is designed to be appropriate for the round and the stage of the business. They keep it simple. It feels like they really understand that.

Co-founder & CEO, Pluto

How do I get all the businesses I invest in to use SeedLegals?

Angel Investor , The Family

It's easy to forget about the legal side of things but SeedLegals make things really easy to understand. The team at SeedLegals are truly amazing.

Founder, TRIM-IT

There’s an opportunity to reach a specialist advisor via chat, phone and email to check in on anything. The SeedLegals team were extremely responsive – really amazing.

Co-Founder, OddBox