Raise smarter: master your fundraising strategy to close your round quicker

Fundraising but not sure what you’re missing? Put yourself on the front foot with these top tips from SeedLegals Bethany...

Already have an account? Log in

Not every startup ends in a big exit. Sometimes, the right move is to wind things down and move on.

Whether you’re closing because things didn’t take off, or because you’re onto something new, it’s important to shut down the company properly – for your investors, for HMRC, and to stay legally compliant.

In this article, we’ll explain the main ways to close a UK limited company, and which is the best option for you.

There are three main ways a UK limited company can be shut down:

If your company is solvent, you can apply for strike-off if:

If you meet these conditions, strike-off is likely your best route. That’s because it’s the easiest and cheapest of the three options (we’ll go over how you actually do it below).

It’s meant for companies that aren’t trading and have tied up all their loose ends. So, if you still have debts, disputes, or recent trading activity, you’ll need to consider MVL or CVL.

If your company is solvent, and still has a lot of money or assets – typically over £25,000 – it might be better to close through a Members’ Voluntary Liquidation (MVL) instead of using strike-off.

That’s because money taken out through an MVL is usually taxed as capital gains (normally 18% or 24%) rather than regular income tax (which can be up to 45%). You might also qualify for something called Business Asset Disposal Relief, which can bring your Capital Gains Tax down to just 14%.

But MVL is a longer, more formal process that requires hiring a licensed insolvency practitioner. Since you’ll probably have to pay somewhere between £3,000 and £5,000+ in fees, it’s only worth doing if you’re taking out a big amount of money as you close the company.

If your company has debts it can’t pay, you can’t strike it off or use MVL.

Instead, you’ll need to:

This is a much more time-consuming and expensive process (you’ll have to pay thousands in insolvency practitioners’ fees).

Occasionally, if the company has no assets and it’s unlikely that creditors will take action, you can still try to strike off the company. But creditors can object and stop the process, so it’s a risky route.

Yes. If you’re not ready to shut the company down permanently, you can make it dormant.

To do this, you’ll need to:

This option essentially lets you “pause” the company and restart trading later, though you’ll still need to do some basic filings.

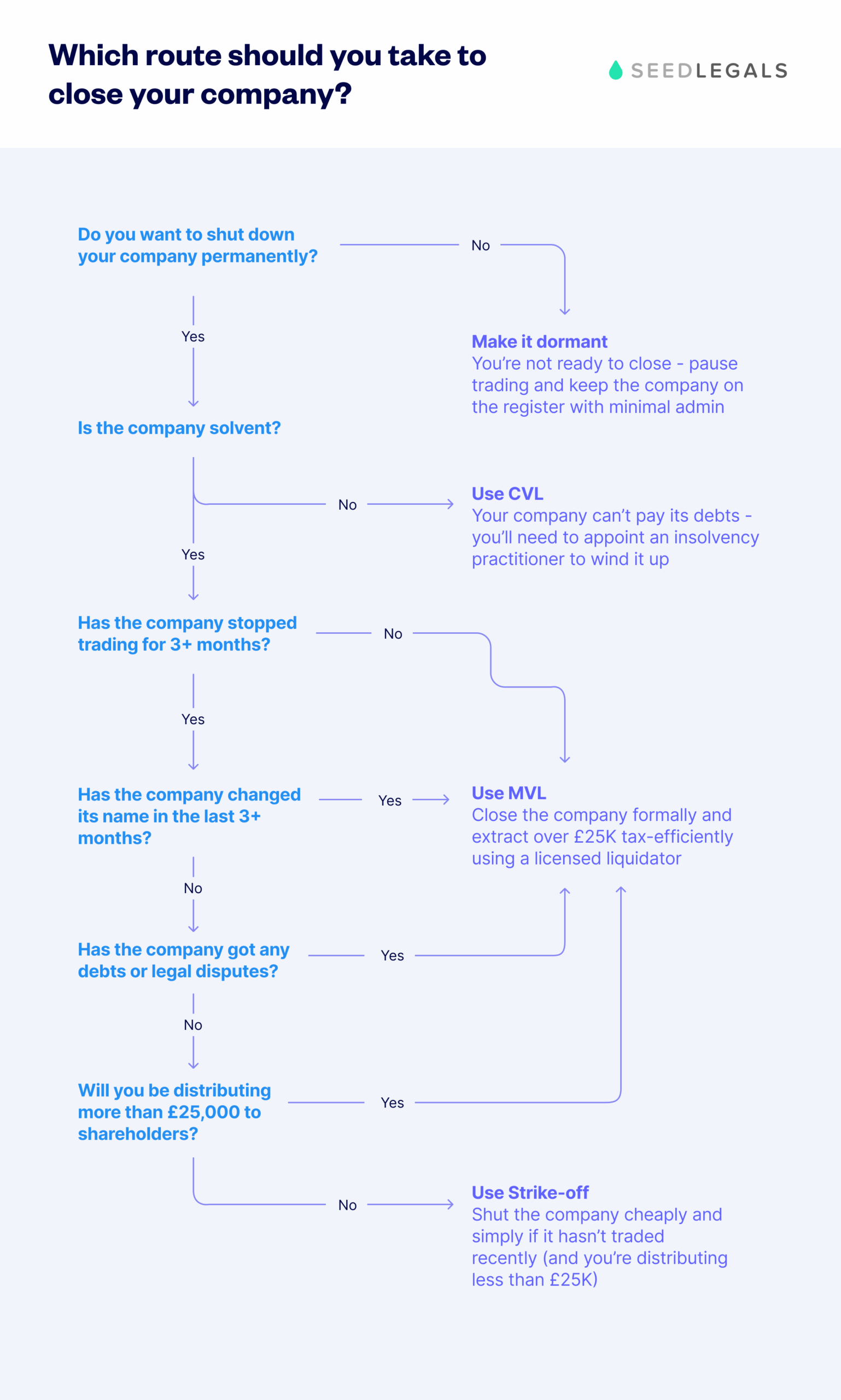

If you’re not sure which option is right for your company, this flowchart breaks down the different routes based on your company’s financial position and what you want to achieve.

If you’ve decided strike-off is your best approach, you’ll need to first close things down properly and tell the right people.

Make sure all company assets – like cash, stock, domain names, and IP – are sold, distributed to shareholders, or transferred to a personal account before you apply. If there’s money left in the bank account when the company’s dissolved, you’ll lose access to that – so make sure you empty the bank accounts. Anything left in the company (and the bank account) at the time of strike-off will go to the Crown (yes, really).

Make sure you:

You must tell all parties affected by the closure within 7 days of applying for strike-off:

If you don’t notify these people, it can result in a fine or even prosecution.

Here’s the step-by-step process to remove your company from the register:

Once received, Companies House will:

From that point, your company legally stops existing.

So, you can see how (if your company qualifies) strike-off is the simplest and most affordable way to close things down.

Whether you’re striking off or liquidating, getting the process wrong can cause problems with investors, HMRC, or Companies House. If you’ve reached the end of the road with your current business, take the time to close things properly and protect your future opportunities.

And if you’re thinking about what comes next, you’re in good company. Our newsletter is packed with insights, resources and real talk from other founders navigating the highs and lows of startup life.

Sign up to our newsletters and get the best of SeedLegals events , insights and resources delivered directly to your inbox.

Article Sources

gov.uk | Closing a limited company – (last accessed 22/07/2025)

gov.uk | Strike off your limited company from the Companies Register – (last accessed 22/07/2025)

Fundraising but not sure what you’re missing? Put yourself on the front foot with these top tips from SeedLegals Bethany...

Pitching isn’t just about telling your story – it’s about convincing investors to believe in it. In this webinar, experi...

Discover how small, consistent decisions compound over time to shape startup success. In this webinar, Anthony Rose and ...