Read transcript

Anthony

Hello everyone.

One of the biggest challenges that founders have apart from growing a team and finding product market fit is finding investors.

And the number one thing that we get off at Seed Legal is: how do I approach investors? How do I decode their feedback? They’ve told me I’ve loved what you’re doing. Come back later.

Or do I need a warm intro? I don’t know anyone. Where do I go?

So today I’m delighted to join with prolific investor Marc Cohen from Unbundled VC, who is well known for giving great and honest feedback.

I will play the part of the founder looking for investment.

And Marc is an example of a great investor, and he’s gonna tell you after how to pitch him later, who’s gonna tell you the secrets of what investors are looking for, and the incomings that they’re actually gonna respond to.

And also we’re gonna tease out how to decode that investor feedback so that hopefully after the session you are better prepped to go off and, once you’ve found investors, pitch and get investor interest. So without further ado, Marc over to you.

Marc

I’ll do a very quick run through on my background, but before I do, I know you know quite a lot about this subject as well, Anthony. So when you ask me your questions, and I know you’re doing it as if you were the founder, please chime in and, and give your feedback – if it’s the same or even if it’s different to what I think.

So, my brief background: a long time ago I was a maths undergraduate. I went into financial markets. I was an interest rate swap trader at banks for seven years. In 2001, I quit and did a master’s in AI at a time when there wasn’t much around. I found a great course at Sussex University in Brighton. I met my wife there who was doing her undergraduate.

So hung around till she’d finished, went back into financial markets, joined a small proprietary trading group, built the systematic trading side of that up from scratch to become most of that business. I had been doing a poker and AI side project, brought my friend I was doing that with in to the trading business.

And we built the fully AI version of that trading system. And we’ll come back to the AI topic a bit later, I believe.

I lived in Logano in the Italian speaking part of Switzerland for the last eight years of that. Then moved here to Guernsey, where I’m based now with my wife and four sons. So that also keeps me busy, as you might imagine.

I started doing some angel investing, became a partner at a small VC out here, and a year or so ago, quit that to see what I could build myself and to invest my own money. and that’s what I am doing now. And there’s definitely a few familiar names in the chat, today.

Anthony

Right. Brilliant. And I saw Marc pop up frequently on deals done on SeedLegals, and so I figured, yes, let’s get together and do a brain dump for everyone.

All right, so we’ve got a packed set of topics we’re gonna go through and hopefully covering all those things that you’ve got in your mind as a founder about reaching out principally to angel investors, but then later on to funds as well.

So the very first thing is finding the right investor.

So a common problem that I see is you just personally don’t know any angel investors.

So you get on the internet or you go to SeedLegals website or somewhere with all those lists of investor directories, and then you write to vc. And maybe they answer and maybe they don’t, but it turns out that they’re only gonna invest once you’ve got revenue, and that’s much later and you need to go find angel investors.

So Marc, give us a quick thought about finding the right investor for your stage of the business. Let’s say at, you know, before you’ve raised your first round, raising, you know, it’s 200 K or so, and then raising a seed round of, you know, five, 700,000 pounds afterwards.

Marc

So I think the the most important piece of advice is you just need lots of tops of funnel. ‘Cause you’re gonna get lots of no’s, right? And particularly in the current funding environment, which is what specifically we titled this, it is harder to raise.

And even if you are like the most exceptional startup there is, you’re still gonna get way more no’s than you’re gonna get yeses.

And that means you need enough people at the top of your funnel to get to a yes. And if you are very fortunate, you might have those in your network and in your family and friends, but most people don’t have that situation.

The best way really, I think is to network with other founders actually. And just get yourself into a group of founders and share experience, share contacts and they will help you and go, I pitched these people, they invest, they didn’t invest, for example, they are good to work with and I recommend that you go and speak to them.

It’s quite hard to actually go and find lists of angel investors and hit them cold. You can do it on LinkedIn and just search by investor and go through and do that, but you just don’t quite know what you are going to get.

And particularly with angel investors, they don’t typically have a website saying, this is what I do and what I’m looking for. And so, yeah,

The short answer is it’s not easy. I’m not gonna claim that it is.

Anthony

Well, of course we keep reading, you know, investors love a warm intro, which is great if you can find someone to do a warm intro. Somebody who, you know, who knows that investor. But the problem is most people don’t.

And so, you know, you either get a warm intro or you do a cold outreach or you don’toutreach at all.

So tell me, you know, how do you see most of the incomings you get? Are they people writing to you cold or is it somebody who knows somebody who says, Hey Marc, can I introduce you to so and so?

And then we’re gonna jump into the perfect outreach for both of those.

Marc

I get a mix. Often it’s from another founder that’s been through my process and they’ve said, oh, you should go talk to Marc. And often I don’t even know whether it’s that other founder.

So my most recent investment was in Mika Vi at Run Yourself. And that was done on SeedLegals with a SeedFAST. One of her angel investors had pitched me previously, but it was still cold. He didn’t actually make the introduction, she just came in through my process and we’ll talk about that later.

Personally, I don’t mind if it’s cold or if it’s warm, if I’m honest.

Most warm intros are just, you’ve persuaded someone that knows me to make an introduction, and it’s not necessarily the same as them going, oh, they’re incredible and therefore it makes that much difference to me.

So I think it’s get a warm intro if you can. And if you can’t, you know, there’s not that much downside in reaching out anyway.

Anthony

Exactly. And I, I think, you know, most people, most investors, at least the ones you want are basically nice and want to be helpful.

And, you know, when people write to me saying, you know, can you look at my pitch deck? And you can you help? I mean there are only so many hours of the day, but if somebody’s taken the time to do a bit of research and references something relevant to me, generally you want to be nice.

I think that’s the way to do cold outreach: get on LinkedIn, you read something about it, you may find, by the way, a top tip is you can find companies perhaps in your area, you can look at them on company’s house, you can look at their last confirmation statement, the one that says with updates, and you’ll get a list of all the investors. And then if you might see that person’s an investor, maybe you can use Crunchbase, maybe you can, you know, you want some factoid that has the scene as the person did some work to find you. And then I think there’s a good chance that they may respond.

So Marc, let me ask you about that. Then also this adage that don’t ask for investment, ask for advice. I think that’s a bit me. So what do you reckon on ask for investment to ask for advice?

Marc

I’m gonna come back to the previous point about the company’s house is really good because I think if you get a personalised approach on LinkedIn, and I’ll tell you what works for me.

If someone just sends me a connection request and that’s it, I typically just ignore it. If someone sends me a connection request with a message, I will look at it. And if that message has obviously been personalised rather than it looks like a message that could have been sent to a hundred people and it’s that generic, it makes a difference. And if it said, oh, I can see you are an investor in this, we’re in Aja in an adjacent space, I was hoping you would understand the space or whatever those words were. I think that makes a huge difference – whether that’s via email or via that outreach on a LinkedIn.

In this case that adage is often true, right? Ask for advice and get money. And the other way round, in this case I think most investors they wanna know and it feels a bit kind of icky if someone has gone, oh, I’d really, can I have a call for some advice? And then actually they’re asking for that really, that they’re pitching you. It’s not the great first impression that you are gonna leave.

Anthony

Right? Cool. And I think, by the way, on the outreach now outreach to investors is very much like outreach to customers. And, you know, in a larger company like at SeedLegals, you’ve got a function called SDR Sales Development Representative. And their goal is outbound, lead gen. And they will typically use LinkedIn and they will typically have a three or four step sequence. The first one is either just a straight connection request with no information, or sometimes there’s a connection request with a message. And there the goal is always to find this icebreaker line, Hey, you were at this event together, or I see you invested in this.

So your investor outreach, I think is exactly the same as your customer outreach. You’re not going to get the investor to invest from the first LinkedIn message. The idea is to get the second date from the LinkedIn message and on the second date you’re not gonna send them a pitch deck, yet you’re going to engage.

So tell me then about this dating sequence. Marc, the one that works best, you know, at what point is it from, Hey Marc, I see you’ve invested in something in the space through to can we meet for coffee? Well, no, I’m in Guernsey. I’m not actually gonna meet you for coffee.

What’s the sequencing to sending the slide deck or getting on a call and do you wanna see a slide deck before call or do you want to just have a little bit of information and then a call, let’s get through the dating sequence.

Marc

I’m slightly unusual in my process, so I might not be the best placed person, but I’ll try and give the advice.

But it’s basically a sales process. That’s exactly what it is. And it’s probably enterprise sales, which means you are not sending out your like a thousand emails that are all identically worded. There’s a different sales process depending on the size of clients that that you’re trying to land.

One thing you wanna do in that sales process actually is rule out the people that aren’t right. Or you you wanna do some sales prequalification so that they rule themselves out if actually they’re not going. So if you say we’re at this stage, don’t be afraid to say that because otherwise you might waste half an hour or an hour on a call with someone who isn’t going to invest in you, right?

There’s always a temptation to maximize the number of calls. But actually you need to manage your time effectively.

I ask for a video pitch rather than a pitch deck. And then I make a decision on if I want a meeting. And if I do, I say send me the pitch deck, but probably I’m only gonna skim it beforehand, because I like to hear about it in your words first.

That’s not the process for most people. I would actually, in that first outreach, I think it’s actually fine to stick that pitch deck in straight away. Because if they’re not interested, they’re not interested, right?

Give them some information to make a decision on rather than keep it vague is my view.

You can potentially get some buy-in, by asking upfront would you be interested in seeing the pitch deck? And then if they say yes, they will feel committed to spend more time than they would otherwise.

But then you’ve gotta get that message of what those first view lines are,those bullet points to capture their attention.

Anthony

So I always love doing things differently and I love the idea of a video. Some people present better and are great at video presentations and some are not, right

What would you like the request to be? I created a one minute video, check it out, we’d love to talk further.

Marc

So I have a use a platform called Willow which is actually a business that I’ve invested in that asks you to do it. So I’m not asking for some professionally produced, video to be honest.

If it looks, if it looked too slick, that’s almost a problem. But also don’t be in the scruffiest room that you’ve been in. Just be sensible, but no one’s looking for something that’s like crazily produced. Try and avoid yourself being in like a silhouette against a light background. I would say.

That idea that some people present better and some people don’t. My view is that sales is such an important skill in a founder. There’s a strong correlation between people that present well on video and those that can sell. And so it’s a way for me to get a feel for that skill before we’ve met.

That’s a really, really good point. I think founders often think there are two distinct things: selling to customers and raising from investors. And the pitch deck is all about, you know, blockchain and other things.

But I think that as an investor, you look at the sales pitch that founder’s doing to you and you extrapolate that to the way they’re gonna sell to customers. And if they can’t sell themselves to you as they would to a customer, then you think they’re gonna struggle with forever building things and not being able to sell it

So now we’re gonna switch to investor personas. ‘Cause one of the things is there’s no single type of investor. Marc’s said several times, that’s just me. So a while back I did a sort of a Buzzfeed style article, What type of investor are you? It’s the SEIS seeker, the spreadsheet scrutiniser, the philanthropist, the hobbyist and the aspiring founder.

Of course, you’ll only have one pitch deck but as you’re talking to somebody, you’re gonna modify the pitch to tap into the things that they’re looking for. Either it’s focusing a lot more on the business plan or focusing on the do good credentials or getting in early

So Marc, how does that apply to you and which one or more or other of those are you?

Marc

None of the personas were particularly complimentary, so I’m not sure I really wanna identify with any of them.

I’m not an SEIS investor, because I live in Guernsey, so those tax advantages don’t apply.

I’m primarily investing because I wanna make money on those investments. That is the first primary thing, otherwise I’m risking what I hope will be my children’s inheritance and I want that to be like way bigger than it would be currently if everything goes well.

But I do care about underrepresented founders and about impact. Those things do make a difference to me. But primarily it has to be that I’m doing this because I think it’s the thing that is gonna have the good outcome. Am I spreadsheet guru? I guess I was a maths person at one point. I want the unit economics to make sense but I’m not gonna spend like on time in that 4,000 line.

I don’t think I’m ever gonna be one of the cool kids.

In terms of helping, the thing that I always say is that because I’m I’m not leading deals, I’ll be anywhere from that frictionless investor to someone that you’ll lean on.

Typically if you do have a lead investor, be that a super angel who writes a larger ticket or when you get to the stage where you get a fund involved, you are going to lean on them a bit more and they are going to want to be involved. You need to make sure those are people that you’re gonna be quite comfortable and happy spending quite a bit of time with over what could be the next five or 10 years

Anthony

Alright, so you mentioned, lead and follow investors.

So this is a trick that most people only learn later when they’ve wasted a lot of time talking to the wrong people, and getting stuck in a loop.

So for everyone: some investors lead deals, they’re the ones who’ll set the valuation, set the deal terms. Others will follow, wait for somebody else to set the deal terms and come in and this becomes a big catch 22 ’cause only a small fraction of investors are want to lead a deal

And so what happens is you talk to many investors and they go, love what you’re doing when you’ve gotta lead, call me. And in your mind – and sorry if I’m a bit negative on many investors, Marc – but in your mind these investors go around saying, we recognize talent, we want to build the future. We are innovators, we are brave. And then at the end of it, go, who’s the lead? And then, I’ll follow if there’s a lead.

So let’s talk about how we break through that impasse.

And by the way, when investors call me at SeedLegals and I get on a call, I start the call by asking the investor to tell ’em about themselves and also importantly tell me if they’re a lead or a follower investor

And if they’re a lead investor, I’ll lead the conversation to try and close an investment potentially on that.

And if they’re follow investor, it’s like keep them warm and when I’ve got a lead, I’ll come back later, but I know how to spend my time accordingly.

So, the problem space is here and then we’re gonna explore this, Marc.

1: Establishing lead or follower

If you’ve got lots of follow investors, can you keep going without a lead? And then can you use seed fast or advance subscription agreements or safes to get outta that impasse

Just so everyone is aware, the purpose of a lead investor, once upon a time had been to do all the admin paperwork and get all the signatories and so on. That’s passed with platforms like SeedLegals: it’s all electronic, but the lead is making the biggest risk by sort of saying I am in, they might be the majority of the round, they might be smaller in the round, but they’re also setting the terms and the valuation and often others, even ones like Seedcamp who you think would do this a million times say we don’t lead, we follow

As the investor, Marc, tell us a little bit on your side about lead versus follow: when would you lead, when would you follow and what would you do?

I know that you jump in with SeedFAST sometimes, so you obviously do get through the catch 22 by coming in early.

I think once you’ve got investor interest, you need to get through the next thing as quickly as possible

I 100% recommend SeedFAST for people because it is just so easy and frictionless to use and it’s becoming an accepted standard in the industry. So people are just very, very familiar with it

In terms of me, I very rarely lead. I had a situation, earlier this year where I sort of ended up leading in a non-lead round just because I was the largest individual ticket rather than really I was the lead. So there was some involvement in sorting out the terms and valuation and those kinds of business but it was almost more sort of arbitrating between some of the other investors and the founder. It depends on your round.

If you have an angel round, there’s no leads. You are gonna go, this is what I want the valuation to be and they’re just gonna say yes or no. Sometimes they’ll push back and then it’s just a question of you trying to get a feel for if you need and are willing to move the valuation

By the time you get to seed, it’s much more common that you’ll have a lead investor that is a fund and sometimes even a pre-seed that will be the case.

Then there’s two different kind of sets of follow investors. Those that just go where you go, you’ve told them what your target valuation is and they go, yep, that’s fine, I’m in. And then there’s another set as you said, Anthony, which go, I only wanna do this if and when you’ve got a lead

I prefer to be the first type. It’s a strong signal if I go, even though you don’t have a lead, I still want to do this.

And if I was a founder, I would definitely be more inclined to have in my round then the people that just said yes anyway and not the ones that were waiting for.

Anyone that says tell call me back when you’re profitable shouldn’t be investing in venture capital. Really the whole point of like venture capital funding is businesses that have the chance to be, you know, very profitable at scale but aren’t profitable now and therefore they need capital to get there and it’s risky and therefore you give equity capital rather than debt capital. And actually what’s gonna happen is they’re gonna constantly be giving you a hard time on because they don’t understand the nature of the journey that you are on as well.

I think that was definitely the quotable quote from you, Marc, we need to get you to stand in Volga Square with the cardboard thing saying, if you’re waiting for the company to be profitable, you shouldn’t be in venture investment

That is the bane of everyone’s existence, right? When investors say, come back later, and maybe that’s a nice segue to valuations.

When you go to investors, you have to of course come up with a valuation both because that reflects how much equity and also reflects the the risk reward that the investor is getting as your business proves that you can build a team, build a product, a product, get customers, get revenue, the risk decreases and therefore the valuation increases.

So how do you come up with a valuation and you know, from thousands of rounds on SeedLegals, it seems that there are distinct buckets

I’ve got a couple of founders and some people together, I haven’t built anything yet.

Or I’ve built something and it’s about to launch, I have launched, but I don’t have users.

I’ve got users and I’m doing 10 K a month revenue.

I’m doing a hundred K revenue.

And so you might see those as almost five different categories.

Marc, when you look at valuations, do you put them into similar sized buckets? Is there much flex if they have the word AI in it, does it get extra zero on the end or that lasted like for three months and now it’s over?

Because to me, one of the key things is in an early stage, no one really knows the valuation, but you see as an investor, lots of companies coming by and if most of ’em are going 2 million, 2 million and there’s one going 5 million, either they’ve got way more traction or there’s just a mismatch and you know, you’re out

So over to you on the valuation conundrum.

Well firstly I’ll just say valuation is just really, really hard. And it’s hard enough sitting here as an investor that sees hundreds of things a year and it’s even harder for a founder to figure out what it is because the things that you see in public that are on TechCrunch, you know, they’re often the hottest deals. They’ll be the things with the highest valuations and you go, well, I’m as good as that, therefore I should have this, you know, same progress, I should have this thing. It’s really, really difficult

The thing I would suggest is that you’ve got, again, to talk to as many other founders that have been through this process as possible. Find out where they were able to raise or where they think you should be able to raise and just talk to as many people as possible.

If you can get advice from some investors as well, that’s helpful. But then, you know, we’re always a little bit biased because if we want to invest, we obviously want to invest at a slightly lower price rather than a than a higher price. So just be aware of people’s incentives as well

The other side of it is the part of the valuation that comes from assessing the founder’s strengths. That kind of doesn’t really come out in any of the metrics.

How much more would I pay to invest in one rather than the other? I’m not gonna pretend I even know the answer to that. I kind of have an intuitive feel for it. Again, it’ll be different for every investor. And the other thing then is obviously you’ve got, you know, what does that path look like? How big could the business be? How fast could you grow?

I have a huge amount of sympathy with founders and unfortunately there isn’t an asy answer.

The one thing I would say don’t do is there are some advisors out there, you know, accountants or whatever that go, Hey, I know how to give you a a valuation, come to us and we’ll give you like a proper venture capital valuation.

Those people do not know and it’s never a good sign if someone comes to you and says, Hey, I had this valuation independently verified. It doesn’t mean anything if it’s not from someone that’s prepared to give you some money.

Anthony

Well that is a great point and I must say I see it as a negative when somebody’s gone, to some accounting firm because they have no idea how investors really value things. I mean, you can certainly use, you know, websites like Quida and others, but the problem is it’s the garbage in and garbage out. So you know, it says enter your revenue projections and you go, great, I’m gonna doing a hundred million a year in revenue by year five. And then it goes, your valuation’s 27 million or something. You go to investors and you tell them 27 million and they go, great, what have you built so far? And you go, I’ve got this, Figma mockup. And they go, you’re out of your mind. So I liked your thought about, you know, reading TechCrunch. I always joke, read TechCrunch and then take at least one zero off the end because those are crazy US valuations and the only ones that ever make it as a story are the ones with a super high valuation.

So they’re all really depressing as a founder, you keep seeing people raising at giant valuations and you know that it’s nothing related to what you can do. And if you’re enticed to go, great, I’m gonna raise in my first round of 10 million, you know, you just find investors, not replying ’cause there’s a mismatch or saying come back later.

So it’s a tricky one Now, and and by the way, I also joke about going to your accountants. ’cause your accountants will say, you know, are you making revenue? And you go, are you profitable? And you go, no. Are you making revenue? No. Are you losing money? Yes. So why is your valuation more than zero? Because accountants value on pre previous financials and investors on future potential.

So Marc, if you were to say, if I were to put you on the spot and go, what are the two biggest peaks in terms of, you know, bucket sizes, amount raised and valuation, would you be able to do a quick cluster analysis in your mind, and go yes, the biggest peak is people raising this amount at this valuation, at this stage, and this amount at that stage?

Marc

I’m gonna say no, I think there’s more gradation because it really, and I know that’s not the answer that’s helpful, but there is a gradation anything from, you know, smaller, like you say 200 up to like seed rounds that typically do have a funding that can be kind of two, even pre-seed that can be like 2 million plus depending on, you know, someone really likes it. And one of the sort of bigger pre-seed funds come in the larger valuations usually have

So the larger rounds usually have larger valuations, but it’s not linear the way that that works. Really I’m gonna dodge that question. I think I’m gonna answer that question that’s just in the chat if that’s okay.

Anthony, isn’t there a downside to having too high valuation?

I think the answer there is yes. The main downside is that when you come to your next round, you can sometimes have made good progress. So theoretically, of course, to minimise dilution, you always just take the highest valuation you can. The risk is you come to your next round, you’ve made good progress, and so you’re like, well, we’ve made good progress, we’ve hit on metrics or got pretty close to it. ‘Cause often the targets are quite ambitious. You go raise another round, you are able to raise another round and those investors go, but I’m gonna give you the money at this valuation and your existing investors go, what the hell? No, you have to raise a minimum of this or we are not gonna accept it because you’ve done great since then and we gave you money here. And that can be a challenge. Now, most rounds that’s not a problem. But if you go too high and sometimes if you are really good at sales, and it’s a purely angel round and sometimes those angels aren’t as well informed, you can get a really high valuation because you are good at sales and, you know, maybe it was less informed investors. But that is the challenge. Then if you bring professional investors in later, you’re gonna get like this, like awkward tension in the middle.

So I think you’ve put it beautifully, my summary of that is in your first round you’re selling the vision and later on you’re selling the actual. In your first round you’re selling the vision and later on you’re selling the actual. So we can use AI to transform the way people find houses and it’s a trillion dollar industry and so on.

If you do a good spiel, people go, that’s awesome. And then they’ll jump into your 10 million valuation and then you use that and, and you launch the product and then your next round comes along, you build a team, you burn 200K a month or 500K a month or something like that and you’re out of money in, you know, eight months. And investors go, great, what’s your revenue? And you go, 200k A month or how many users you’ve got and you go 27 and then the dream comes crashing down. And of course the other thing is for those investors who think the valuation ought to be lower, then they’re just gonna go come back later.

So let’s now quickly talk about the converse, which is too low evaluation. So if you’ve got a very low valuation, you dilute yourself. But one of the challenges that I sometimes see, is great fundraising is going great, my round is now oversubscribed. I want to raise the valuation.

And if I’m an investor and on a 2 million valuation and the founder then says I’m raising it to three or two and a half, I will be out and I’ll never want to talk to that person again. ’cause I see it as a breach of trust. How do you deal and, and on your side, do people periodically say they want to raise the valuation and is that something you’re amenable to or is it like a I’m out, don’t talk to me again?

Marc

So I’ve, I’ve definitely had this happen before when rounds ended up being oversubscribed. So the way I frame it is I’m making a commitment based on this valuation. If it changes, come talk to me, right? and so then I leave it, I’m making it very clear to them that I’m not saying no, but I did do it on this basis. And if the valuation goes up like 50%, then you know, obviously we’re gonna need to have another conversation.

So there’s a balance somewhere in the middle, but I think you definitely keep all your investors informed as early as possible if you are thinking about doing something like that.

Anthony

That makes complete sense. So the summary is, you know, have a conversation and you may need to be prepared to lose some of the investors, which may not be a problem if you’re oversubscribed.

What you don’t want to do is lose most of it and then you go back to where you started.

Alright, let us switch now to current fundraising climates. You know, a year or two ago, valuation multiples were insane. Once you were a revenue generating company, the valuations you could expect might be 10 to 15 times annual revenue. Maybe it’s now more like six to eight. Do you have an observation there firstly on valuation multiples and then we’ll go onto hot segments. And in between, how would you change your pitch to target investors now compared to the wild days of, you know, I’m raising tons of money and I’ll figure out a business model later.

Marc

The multiples can vary hugely depending. Even now you know, just how attractive the proposition is, how big it could be, how fast it’s growing, you know what your gross margin is, your unit economics, all those kinds of things. So it’s never quite as simple as just here’s a multiple, but they’re definitely a lot lower than they were. And the cliff was kind of around the middle of last year. Like anything sort of June or earlier was at one level, then the market died in July and August and in September people came back in and were not quite, there was a bit of hesitancy as people came back in ’cause they didn’t know where things would renormalize to. So the first thing is it is different. They are definitely a lot lower than they were, although it’s again hard to put any specificity on it. And obviously if you are like very low revenue, that multiple can still be very big because it’s non-zero your valuation when you are at zero, right?

So at some point it goes through a scale and things start to normalise. A challenge interestingly is sometimes, and we talked about this with the, the downside to having two higher valuation is when people’s last round was before the middle of last year, then effectively the valuation, if they’d raised that in the new environment would’ve been lower. And they are in that spot where effectively they started from a really high valuation.

Onto the second half of your question, which is how do I pitch differently now? I think there is more of a focus on the underlying unit economics and correctly. So a focus on the underlying unit economics that if you buy a customer, a customer’s, you know the whole lifetime value to CAC thing that you talked about with your spreadsheet, what people are much more interested in that and they should be more interested in that, right? You’re looking for businesses that at scale can be hugely profitable and underlying unit economics, things like that tell you something about that. They’re also looking for a nearer term path to profitability. And I think that’s a sensible thing to be looking for in this market because otherwise what you can have is a business on the face of it that looks quite good, right? It’s growing at quite a nice pace.

Those underlying unit economics all look sensible. Market size is big enough, you’re doing it the right way. But that’s not always enough now to get funding given the current environment. So you need to know that if that got tough, you’re like, okay, could I raise a smaller round that would get me to profitability if you were doing that? And look, if you’re very early some businesses that just isn’t going to be possible. But it’s definitely more on people’s minds than it was before. Not necessarily because it’s really the best path for the business, but to know that you’ve got a plan B if you are not growing quite as fast as you would like to be. So I think that’s sensible to be honest from founders and from investors to know that there is a chance for that plan B.

I think there’s always been that divergence between I would say UK European investors and US investors that the US are more ambitious. I think it’s contracted a bit, given what’s happened in the last year or so. And probably what’s right is somewhere in between the two of them, because actually venture capital is there for businesses that aren’t profitable now. And it’s probably, if anything in the UK swung back a bit too far the other way. But it is still the reality of the environment that you are in. For me, dilution is not the factor. It’s about like what’s the thing that gets you to the highest value of your shares right at the end? And if that requires more dilution for you to be able to grow faster and still take over the world, then you know that ought to be fine. I think. It’s not about how much you own, it’s about, you know, how big could this be at the end?

Anthony

In the valuation discussion, if you’re pitching to a VC, should you wait for them to propose valuation or is it okay for you to propose valuation? I must say this is one that’s intriguing for me ’cause we talk to VCs, I’ve got a particular valuation in mind. I kind of want to not waste everyone’s time by going, listen, if it’s gonna be less than this amount, really don’t waste my time. I’ll keep looking. Um, but what, what is the, the, the go over there?

Marc

Normal I think is that you come in with a valuation that you are targeting. What then happens in practice is the VC typically says, okay, that’s fine, has the conversation, you don’t hear anything again, and then your term sheet comes through and it usually has a low evaluation on it, right? And, that’s just might seem weird that they don’t mention it upfront, but that is generally what the world looks like. Even before the middle of last year. Now it’s different if you’ve managed to get a competitor environment where you’re getting multiple term sheets coming in and they know that there’s multiple term sheets around, then you might even see some that are higher than you were than you were looking for. Or you might not, even if you know it’s competitive, you might go, I don’t have a target valuation, but most of the time you come in with a target and then a term sheet appears and you’re like, oh, that isn’t quite what I was hoping for. Unfortunately that’s normal. And so the incentive is to like push it a bit higher, and then knowing it’s gonna come a bit lower. But the risk factor is if you push it too high to start with, they’ll be like, Ugh, that means I don’t even wanna talk to them. ’cause I know they’re gonna hate if I wanna do it. I know they’re gonna hate what there is. So again, not an easy answer on that front. I think a pre-seed, which I think there’s a lot of people in the audience that are probably at that level, it is probably more people, it’s more common that I hear, oh, we’re waiting for our lead if we get one to set the valuation. So again, angel rounds typically you’ll set the valuation and you might need to have some conversations led rounds in pre-seed. Sometimes you’ll have a target, sometimes the lead is setting it. And yeah, I don’t have any easy answers for you, I’m afraid.

Okay, so top tip, you know, in any negotiation for those who’ve read the literature, there’s the power of what’s called anchoring. So the first, a number put on the table sets everyone’s mind. If I go to pound land and I see this here fine glass listed as a pound, you know, I’m, I’m unlikely to get much different from it. If I go to Harrods and I see this fine glass of 25 pounds, you know, I, I’m thinking in that zone and maybe I’ll persuade them to go down to 20 or whatever it might be. So if you can, whether it’s selling a product to a customer or you know, engaging with, with a supplier in something or pitching to an investor, anytime you can anchor the discussion, then, that it’s easier to operate in that zone afterwards than them coming up with a low ball figure that’s half of what you had in mind and trying to drag it upwards so you can explore those negotiation techniques.

When you’re in, early, revenue, just getting a bit of revenue, you might be passing the angel investor stage ’cause you’re looking to raise a million pound. That’s a lot of angel investors you might be in a bit early for most VCs. How do you present your revenue? Are you projecting the future? How do you get it to entice that VC that you’re ready for your later stage round?

I think it’s about this is where I am now and this is where I can be in sort of a year, 18 months, two years time. And it’s not just about the words where you go, I’m at my 300 K now and in a year’s time I’m gonna be at 3 million. That sounds nice. And often you hear, and I’ve got all these people in my pipeline and I’m gonna have all these wonderful contracts. That’s a very standard thing that you hear. I’m sure that people believe what they’re saying. So I’m not accusing anyone of dishonesty here, but most of those things, it’s hard to know which ones are gonna happen as an investor and which ones aren’t, right? So try and put yourself on the other side of the table and go, if this really is likely, how can I make it easy for this investor to see that it’s likely, right? How can I evidence that, that actually we do have a great chance of converting our pipeline into real sales? So for example, it might be, do they want to do a client call? The interesting thing about client calls, you don’t want every single one of your investors to do one because you’re just gonna upset your clients.

So either get your lead or one of the larger investors to do it and get them to be happy to talk about it to the other investors, either to write a note on it or even to take calls from other investors if they’re interested. Or what I did for a business was, I actually recorded a client call. They actually ended up using that with their lead. When we had the investor drinks and I met the lead, it was really weird. They said, I feel like I know you already ’cause I’ve watched that client call seven or eight times. But either way you are just, it doesn’t have to be via a client call, but find some way to evidence that the clients love what you do and they have this real need that can’t be served anywhere else. That makes complete sense.

Super important thing, which ironically we’re talking about VCs but now is one for early stage investors, friends, family, how am I gonna get my money back again? How am I going to get a return on investment? Of course, professional investors know that some percent of the companies will fail. Some will sit around in, you know, great companies but not making your money and some of them will exit for a high valuation. Your challenge is you get friends and family and they might ask, can I get my money back in three years or can you guarantee me a multiple? I tell people, you absolutely must never do that because it’s not a promise that you can reliably keep. And any written agreement related to the investment that promises a person a return will invalidate SEIS and EIS. So the person will be worse off for having that if seen by HMRC. So how might you get a return on your investment? Is it through dividends? Is it through sale of your shares in a secondary in a later round, or is it waiting for the company to exit? And then how are you persuaded by a founder that you’re gonna make a return on investment?

If you want friends and family to remain friends and family, tell them the truth because that, you know, not everything is guaranteed to work. And, you know, if everything works, this could be a five to 10 year experience, right? And that you shouldn’t do this unless you are okay with that risk profile. I understand that not everything I’m gonna do is gonna work and that if I get some money back, it’s gonna be at some point in that period and hopefully as much as possible. And so then I apply my usual investment process and that could be a hundred different things and we can discuss that if that’s a follow-up question. But if you are not aware of that, venture capital is for businesses that aren’t profitable now and may not be for some time, you shouldn’t be doing this.

Anthony

Let’s talk about what’s hot, right now and what’s not, which of course, isn’t helpful for most people. ‘Cause if you just tell people, fishing technology is hot, you go, great. That doesn’t help me. I do pizza. So, are there are particular segments that you’re seeing? I mean, it seems that, FinTech B two B SaaS always seems to be a hot area. Have you noticed any hot zones? And then we’ll talk about AI.

Marc

I’d say definitely don’t say you’re an AI business if you’re not. And if you’ve just got an AI chat bot, you’re not an AI business. I see there as sort of three different types of business. There’s the foundation models, the LLMs, which realistically there’s not gonna be many of those. They require like a minimum, like a hundred million to even get started just ’cause of the training costs and the cost of the people that you need. So I think we can almost for this conversation just rule those things out. But that’s the kind of proper deep tech thing. There’s then lots of people building directly on top of LLMs and that space is hot. The, the challenge is that as an investor is that sometimes people are building the same things and you don’t know quite what’s being built. There’s definitely a potentially faster path to revenue there because it is a big jump in the tech in terms of what you can do. And then there’s the sort of shallow ones where chatbot or anything else uses it and that’s gonna be literally every other company in the world using what those stage two built. And maybe some of them are using the stage one for their developers and building just using chat GPT or other tools ’cause it’s helping with, with their software development. But those companies still aren’t AI companies. They’re using the tools that have been built, built by AI companies or they’re using it to speed up their software development, but they’re not AI companies. It’s good to know they’re using them because actually you may be able to build faster if you’re doing it, but don’t misrepresent yourself.

Anthony

I’d love us to talk longer, unfortunately time’s up. How can people contact you, Marc, and how can they pitch, noting that Marc isn’t an SEIS or EIS investor. So if he invests in your company, he won’t eat your SEIS allowance, which will be available to others. So he’s a great investor to pitch.

Marc

Go onto my investment on, onto my website, which is unbundled vc, very easy to find. There’s a pitch button. It will ask you to do a no more than three minute video pitch. Come through and do it that way. If you have a lead investor you can book directly into my diary. Please only use that one if you really do have one. But I don’t mind which way you come through. It’s fine. Two of the four investments I’ve made this year didn’t have leads and two did. And so, you know, the most recent one was cold and I invested in seed fast. So unbundle, vc, see whether you think I’m a fit as an investor and please pitch me if you are. If I am.

Anthony

What feedback, if any, can people expect? Is it sort of like yes, no, or do you give a few words of wisdom?

Marc

I give everybody some feedback. It can be anything from like three bullet points to some paragraphs. But I try and give everyone something that’s useful. It’s obviously up to them whether they think it is or not.

Anthony

Alright, thank you so much Marc. You can reach me either [email protected] or Anthony Rose on LinkedIn.

Anything you need to know once you’ve found investors or to do your funding round, or valuation and more, feel free to ping me and I think both Marc and I, subject to hours in the day, love to be helpful, and provide feedback and, and help others on their journey as well. Thank you everyone.

In this post, we explain the funding hot-spots in the calendar year and how to make the most of them, and strategies to take an investment without doing a full funding round.

Watch: How to pitch to investors – a VC tells all

SeedLegals CEO and co-founder Anthony Rose sat down with Marc Cohen from unbundled.vc to find out how to present the perfect pitch to VCs.

Watch the video to find out how to do cold intros, find the right investors, tell a great story, and get investors on board.

Can’t watch the video? Click below for the auto-generated transcript.

Make the most of the 3 funding hotspots

At SeedLegals, we close one in every six early-stage funding rounds in the UK – more than any other service. From the data we have from all these deals, we’ve observed three spikes of fundraising activity every year:

1. End of the tax year

The weeks leading up to April 5th are busy, particularly for SEIS and EIS rounds. Investors are keen to get deals closed to make sure they get the maximum tax relief in the current tax year.

⚡ Read more: How to close your funding round before the end of the tax year

2. Just before summer holidays

Traditionally, many investors take time off in August. If your deal isn’t done by the end of July, it probably won’t be closed until September or later, hence why founders and investors are keen to complete before August.

3. Run-up to Christmas

This season gets busier for several reasons. Similar to the summer holiday shutdown, there’s a spike in activity as founders and investors race to get all the paperwork done and deals closed before taking a break for the festive weeks.

VCs are also feeling the pressure to tie up planning and reporting before the end of the year.

Another advantage of sorting out your deals before Christmas is that you’ll be ahead of other companies who aim to close in Q1 the following year, before the end of that tax year.

Christian PankuiIt’s important to note that the deadline for filing tax returns is in January. Many investors aim to complete their investments before 31 December to align with this deadline. You can use this to your advantage and increase your chances of securing necessary funds by developing a funding strategy that capitalises on the urgency investors often feel at the end of the year.

There’s another reason that initiating your fundraising round before the end of the year can help you successfully close or even oversubscribe your round. The the funding landscape tends to become highly competitive as the tax year draws to a close in April. By starting early, you can build momentum ahead of other startups planning to kick off their rounds in the first quarter,

Funding and equity strategist,

Resources: where to find investors

- How to find startup investors

- Top VC firms in London

- Most active EIS funds

- How to find startup investors

- Top VC firms in London

- Most active EIS funds

Get your free pitch deck template

Create an investment-winning pitch deck with our customisable template.

Ready to raise? Close deals quickly with agile funding

A full funding round feeling a bit ambitious this time of year? No problem – at SeedLegals, we’ve pioneered a new way of raising. It’s called agile funding, and it’s changed the game for time-poor founders. Why? Because it’s…

⚡ Faster: get deals signed, funds taken and finer details finalised later

💪 More efficient: easier to manage alongside running your business

🌪️ More flexible: forget the all-or-nothing priced round. With agile funding you can take a series of smaller amounts as and when you can, allowing you to grow your business as you raise

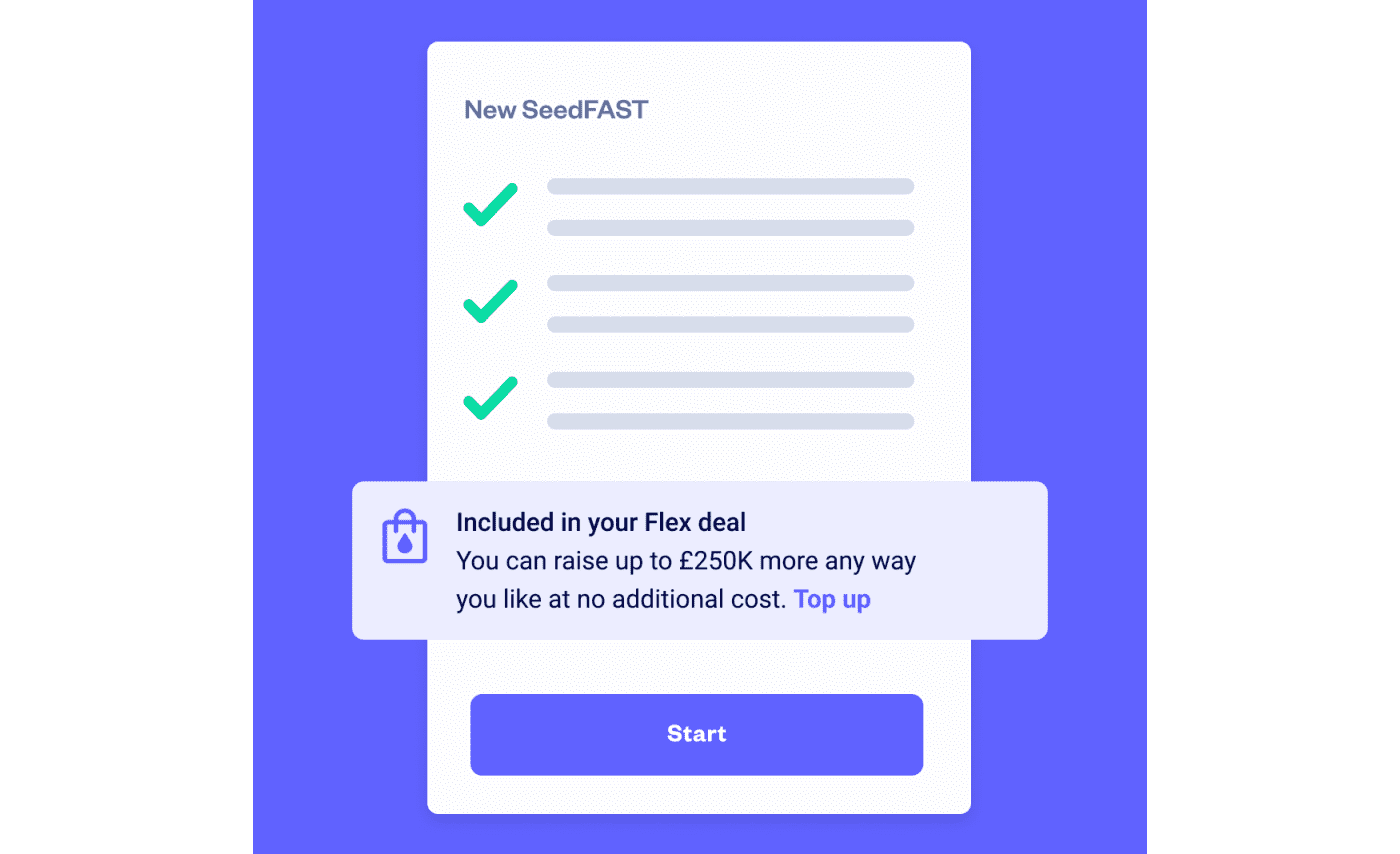

Instead of waiting to line up a full cohort of investors for a priced round, with agile funding you can take in one-off investments. SeedFASTs (our advanced subscription agreement) are by far the most popular way to do this, followed by SeedNOTEs and Instant Investment.

SeedFASTs are the new seed round

In 2022, agile funding became the most popular way for companies to raise, overtaking the traditional funding round structure.

2023 cemented the pattern. In the first half of 2023, 70% of fundraising on SeedLegals took place outside a round.

For more eye-opening investment insights, check out the 2023 funding report.

In 2022, agile funding became the most popular way for companies to raise, overtaking the traditional funding round structure.

2023 cemented the pattern. In the first half of 2023, 70% of fundraising on SeedLegals took place outside a round.

For more eye-opening investment insights, check out the 2023 funding report.

Go agile with SeedFAST

You can issue a SeedFAST (our ‘advanced subscription agreement’) to new investors at any time. They allow investors to sign up to get shares in an upcoming funding round, in exchange for giving you money now.

For a SeedFAST, you don’t set a valuation. Instead, your investors get their shares (usually at a discount) when you close your next funding round. SeedFASTs are carefully worded, easy to understand and – importantly – comply with SEIS and EIS rules.

Because SeedFAST is so straightforward, it’s normal for investors to sign them within 24 to 48 hours of receiving the document. This means you get an instant injection of cash without weeks or months of negotiations. We explain more in this article:

MORE: SeedFAST – how ASAs work

For more complex deals before a round, use a convertible loan note

If you have an investor who’s ready to invest before your round and wants interest or a return of capital, you can use our convertible loan note, SeedNOTE.

☝ Note: SeedNOTEs / convertible loan notes aren’t compatible with S/EIS investments.

Investors like convertible loan notes because if your company is insolvent or looking to liquidate or wind up, debt ranks higher than equity. And this type of agreement gives investors their money back if your company fails to raise a ‘qualifying funding round’.

MORE: SeedNOTE – how convertible loan notes work

Top up a previous round

If you have some investors ready to sign now but some who aren’t, with SeedLegals you can build into your funding round the ability to top up the round after it’s closed without having to get further consent from your existing investors.

With our Instant Investment, you add terms to your round to allow you to close your round when you reach an amount you’re happy with (or the amount you’ve been able to raise right now) and then top up later, within agreed limits.

Bundle and benefit

Save with Flex fundraising

Not sure exactly how you’ll raise? SeedLegals Flex lets you create an unlimited number of SeedFASTs, funding rounds and Instant Investment top-ups for one fixed fee. Valid for 18 months!

Flex my fundraise

Two must-have documents to get ready to raise

If you want to make the most of the momentum to close your fundraising round before Christmas, then it pays to have everything you need lined up – in particular, your SEIS/EIS Advance Assurance and Term Sheet. There’s more on these below

Get your SEIS/EIS Advance Assurance

A first step for many founders when fundraising is to apply for SEIS/EIS Advance Assurance. Many investors will only consider investing in a company that’s got this Assurance because it means they’ll get tax relief on their investment. Advance Assurance sets you apart from other companies as a very attractive investment opportunity. Here’s how it works:

The Enterprise Investment Scheme and Seed Enterprise Investment Scheme allow investors to claim tax relief on the money they invest in your company. Investors can claim Income Tax relief at 50% for SEIS investments of up to £250,000 each tax year. And for the EIS, it’s 30% on investments of up to £1 million.

At SeedLegals, our expert team can review your S/EIS application in three days or less. We can help you get your Advance Assurance fast – our success rate is 98%. Here’s how:

MORE: Apply for S/EIS Advance Assurance

Compile your Term Sheet

When you start fundraising, you’ll need to prepare a Term Sheet: it’s a summary of the investment terms and a very handy tool to have ready when you’re approaching investors.

Here’s why it’s smart to prepare your Term Sheet before you meet investors:

- Know what you’re asking for

When you compile the Term Sheet, you have to think through exactly what you want. This can kickstart your conversations and give you the upper hand in negotiations with investors because you’ll know exactly what to ask for. - Show you’re serious

Investors who put money into early-stage businesses need to know the founders are reliable. By having your Term Sheet ready, you’ll show a level of professionalism that will set you apart from the rest. - Be ready to follow up

If you’ve pitched to an investor and it seemed to go well, it can be frustrating to hear nothing for a week… or a fortnight… If you have your Term Sheet ready, you can follow up by sending over the document soon after your pitch. - Generate some FOMO

When you send your Term Sheet to investors, this can imply you’re negotiating with other investors. Show potential investors you’re keen to move quickly – give them the FOMO (fear of missing out).

On SeedLegals, you can create your Term Sheet in minutes. Select from options for each term (there’s guidance built in) and your document is generated automatically. You can then send it to potential investors via SeedLegals

It’s normal to do plenty of negotiation about the Term Sheet because it includes so many details such as the valuation, vesting schedules, reporting requirements and founder salaries.

💡 Tip: It’s worth putting effort in to get your first investor on board – we’ve noticed that when founders have got this first signature, it’s generally easier to get subsequent investors to sign (and therefore close the round faster).

Talk to the funding experts

Keen to make the most of an upcoming funding hotspot? If you’re ready to make the most of investor momentum, book a free call with a SeedLegals funding strategist today.

Get answers fast, for free

Bring all your questions - we’ve got the answers!

We’ll match you with the right specialist.

Our team of experts is here to help

Bring all your questions – we’ve got the answers! We’ll match you with the right specialist.