SeedLegals introduces SEIS/EIS SAFE for US companies raising investment from UK investors

We explain what US companies need to do to offer SEIS/EIS to investors - and how to use the SeedLegals SEIS/EIS compatib...

Already have an account? Log in

Important news for any UK company looking to raise investment from US investors, SeedLegals’ hugely popular SeedFAST now has an option to match the deal terms expected by US investors looking for the deal terms equivalent to Y Combinator’s Post Money SAFE.

In this article I’ll explain what that actually means, give a quick background to convertible notes and SAFEs, explain the pros and cons of YC’s Post Money SAFE, and show you how to do your next US investment on SeedLegals with our UK version of a SAFE.

In a traditional funding round, the founders round up a bunch of investors, agree a valuation with them, and then the investors get shares in the company proportional to their investments and the agreed valuation. If you’ve managed to round up all the investors to fill out your round and managed to agree a valuation with them, brilliant.

But what if you wanted to raise £500,000 for example, but you have an investor who wants to invest £50,000 now, and you could really use that money now? It doesn’t make sense to do a funding round just to raise £50,000, what if there was a way for the investor to give you the £50,000 now, and you promise to give them shares when you do your next funding round, based on the valuation you agree with the new investors in that round?

Historically, the way to do that was using a Convertible Loan Note. But convertible notes aren’t compatible with the UK’s popular SEIS and EIS tax benefits for angel investors because they offer interest and a return on capital. As a result, convertible notes aren’t popular in early-stage UK funding rounds, where 80% of investment is SEIS/EIS. The solution that emerged a few years ago is known as an Advanced Subscription Agreement (‘ASA’). At SeedLegals, we productised that and call it a SeedFAST. It’s hugely popular, with thousands created by our customers. In fact more investment is now raised before and after a funding round than in a round.

Separately, in the USA, Y Combinator were looking for a way to quickly and easily make lots of investments using standardised deal terms and without the insane US legal fees (SeedLegals isn’t in the US yet…). So they came up with a Simple Agreement for Future Equity (SAFE).

Their SAFE become hugely popular too, and now most pre-Seed Round investments in the US are done by SAFE.

If you’re a UK company raising money from a US investor, chances are high that they’ll ask for a SAFE. At first glance it’s tempting to just download a free SAFE template agreement from the YC website, but you’ll quickly see that it won’t work, for two key reasons:

The good news is that since a SeedLegals SeedFAST is, at root, the same concept as a SAFE, when you have a US investor just get onto SeedLegals and create a SeedFAST for them. Easy.

But wait, not so fast…

The first version of Y Combinator’s SAFE was similar in its key terms to a SeedFAST in that the SAFE converts as if it’s just another investment in the round, at the same valuation as the other investments in that round (plus any discount or valuation cap that you gave your SAFE investor).

But a few years ago, Y Combinator introduced a new version, known as a ‘Post Money SAFE’ – you can read about it here.

In this new version, instead of the SAFE converting at the valuation of your next round (ignoring for now any discount or valuation cap that you may have offered to the investor), if the SAFE converts at the capped valuation (the ‘cap’) then it converts at the agreed cap minus the value of all SAFEs and other convertible instruments.

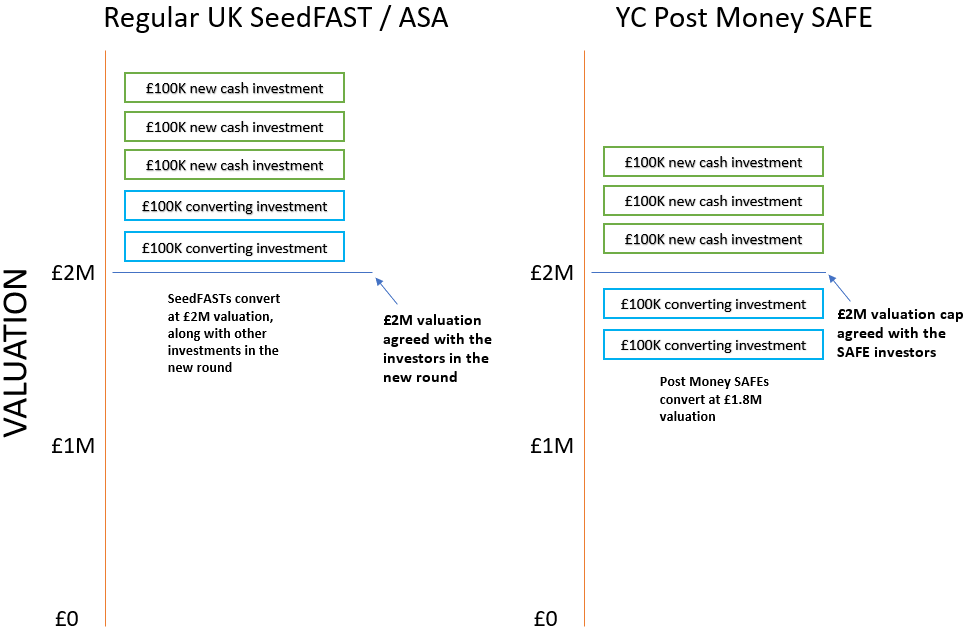

It’s easiest to understand this visually:

To understand the difference, let’s assume you’re planning to raise a total of £500,000 in your next round, of which you’ll raise £200,000 in SAFEs which will convert in your round, and £300,000 in new cash investment.

On the left, you can see that if you did those investments with SeedFASTs, the investments would all convert at a £2 million valuation, and you and your existing shareholders would be diluted by:

£500,000 / £2.5 million = 20% dilution

On the right however, you can see that the Post Money SAFE converts at the valuation cap you agreed with the SAFE investor minus the value of any existing SAFEs and other outstanding convertibles, so in this example that would be at a £1.8 million valuation.

This means you’re now diluting by:

£200,000 / £2 million = 10% for the SAFEs

£300,000 / £2.3 million = 13% for the new investments

for a total of 23% dilution

Y Combinator’s use of the term ‘post money’ is deeply confusing and leads many founders and investors to think they’re signing up to something that’s very different to what it turns out to be!

Normally the term ‘post money’ means the valuation after your funding round.

For example, if you’re raising £500,000 on a £2 million pre-money valuation, then the post-money valuation (the valuation at the end of the round) is £2.5 million.

But when it comes to a YC SAFE, post money means something entirely different: it means the valuation cap (that you agreed in the SAFE) minus the value of all SAFEs that are outstanding and/or converting in the round.

So YC’s use of the term ‘post money’ means ‘post the value of the converting SAFEs’, rather than ‘post the new investments in your next round’… which is very different to what most people are expecting.

When you create a YC SAFE, you can configure it to convert at a discount to the next round valuation, or at a capped valuation.

In the US, SAFEs typically don’t have any longstop date – it may be years before they convert in a future funding round, or even (crazily) never convert at all if you never do a new funding round. But in the UK, it’s typical that SeedFASTs have a longstop date, and if you haven’t done a new funding round by the longstop date then the SeedFAST converts at the specified longstop valuation.

If conversion is at the longstop valuation, then it converts as per 1. above, it’s simply at the agreed valuation, there’s no ‘post money’ subtraction of the value of the outstanding convertibles.

When you create a SAFE or SeedFAST. you can set it up so that when it converts in a new funding round, it either converts at

(You can also combine the two, so the SeedFAST converts at the lower the next round valuation less the discount, and the cap)

So, which method should you use?

In the UK the normal use case is a discount to the next round valuation. That’s because in the UK typically SeedFASTs are used as bridge finance ahead of the next round and the idea is to convert them in 6-12 months, so you’re really offering the investor a modest discount for coming in early and taking some additional risk.

But in the US it’s different, and the normal use case is a cap. The reason is that in the US, SAFEs are used instead of the next round, so years might go by and then you have a monster round at a $50M valuation. So in that case investors look at the cap as representing the valuation today, which their SAFE will then convert at potentially years later.

Choosing a cap that’s too low can be a big mistake, you could end up giving your SAFE or SeedFAST investor way more equity than you had planned, if your next round is at a much higher valuation than the cap. Which is why we suggest going with a discount, unless your (typically) US investor insists on a cap instead.

Y Combinator has its own rationale for doing things this way, but the usual way to justify subtracting the value of any SAFEs and other converting investments is that if you raised money months beforehand with SeedFASTs or SAFEs you’ve probably spent that money already, so pretending it’s new money isn’t right. Because you have an obligation to convert it, an investor could put the case that you should therefore regard it as a liability rather than an asset, and therefore include it in the new round valuation on an as-already-converted basis… which means converting it at a lower valuation.

Y Combinator has a webpage with background and reasoning, but it’s pretty impenetrable to any UK founder or investor. Basically, US funding rounds are very different to the UK:

If you’d raised $1 million in SAFEs which converted at a $20 million valuation cap, it would make little difference if it converted at $19 million instead.

But, if you raised £500,000 in SeedFASTs and that converted at £1.5 million instead of £2 million cap, that’s a major unexpected dilution.

And that’s the issue with Post Money SAFEs, they can be dangerous because they can lead to more dilution than founders were expecting.

Take the following scenario:

With the normal UK way of converting those SeedFASTs, they would all convert at the agreed £2.5 million valuation cap.

But, had they been done as YC Post Money SAFEs, they will convert at a valuation of £2.5 million minus £300,000, diluting Jill more than she had originally planned.

If you’re able to predict up front the amount you’ll raise by SeedFAST, and you factor that into the agreed valuation cap, great, the Post Money SAFE is fine. But if things don’t go as planned and you raise way more with SAFEs or SeedFASTs, Post Money SAFEs can turn out to cost you a lot more dilution than you had originally planned, so you need to be cautious.

If you’re a UK company that needs to create an investment agreement for a US investor that’s asking for a Post Money SAFE, good news, you can do that on SeedLegals in a few clicks.

Just create your SeedFAST as normal, then in the deal terms select the Y Combinator Post Money SAFE option.

By selecting this option, you’ll get a document that’s in English law, with similar language to a regular SeedFAST (so it’s compatible with your next round) but which provides the Post Money conversion wording that matches the YC SAFE.

By the way, our Post Money option works fine for UK investors who ask for YC Post Money deal terms. But we recommend pushing for the standard conversion because it’s – ahem – safer.

We explain what US companies need to do to offer SEIS/EIS to investors - and how to use the SeedLegals SEIS/EIS compatib...

New data shows the way that startups are raising investment is changing, and SeedLegals is pioneering that change.

Watch our founder and CEO Anthony Rose on stage at Slush 2021, as part of the Builders' Studio series. In 26 minutes, A...