US taxes and reporting: What founders need to know

Starting a company is exciting – but alongside the challenge of building your business comes the task of keeping on top...

Already have an account? Log in

When you’re raising money for your company, the stock you’re offering are ‘securities’ – they’re financial assets giving investors a stake in your business. The Securities and Exchange Commission (SEC) regulates the sale of securities to protect investors. Normally, selling securities publicly requires a formal registration (which can be time-consuming and expensive) – and early stage companies don’t want to go through it.

That’s why Regulation D was introduced. It offers companies a way to raise money privately without needing to go through the full SEC registration process. Rule 504, 506(b) and 506(c) are three exemptions under Regulation D that let companies raise money without registration, but with conditions to still protect investors.

So, as a founder raising money for your company, you’ll probably need to choose between these exemptions under Rule 504, 506(b) and 506(c).

In this article, we’ll explain the differences between each of them, so you can make the right decision for your fundraise.

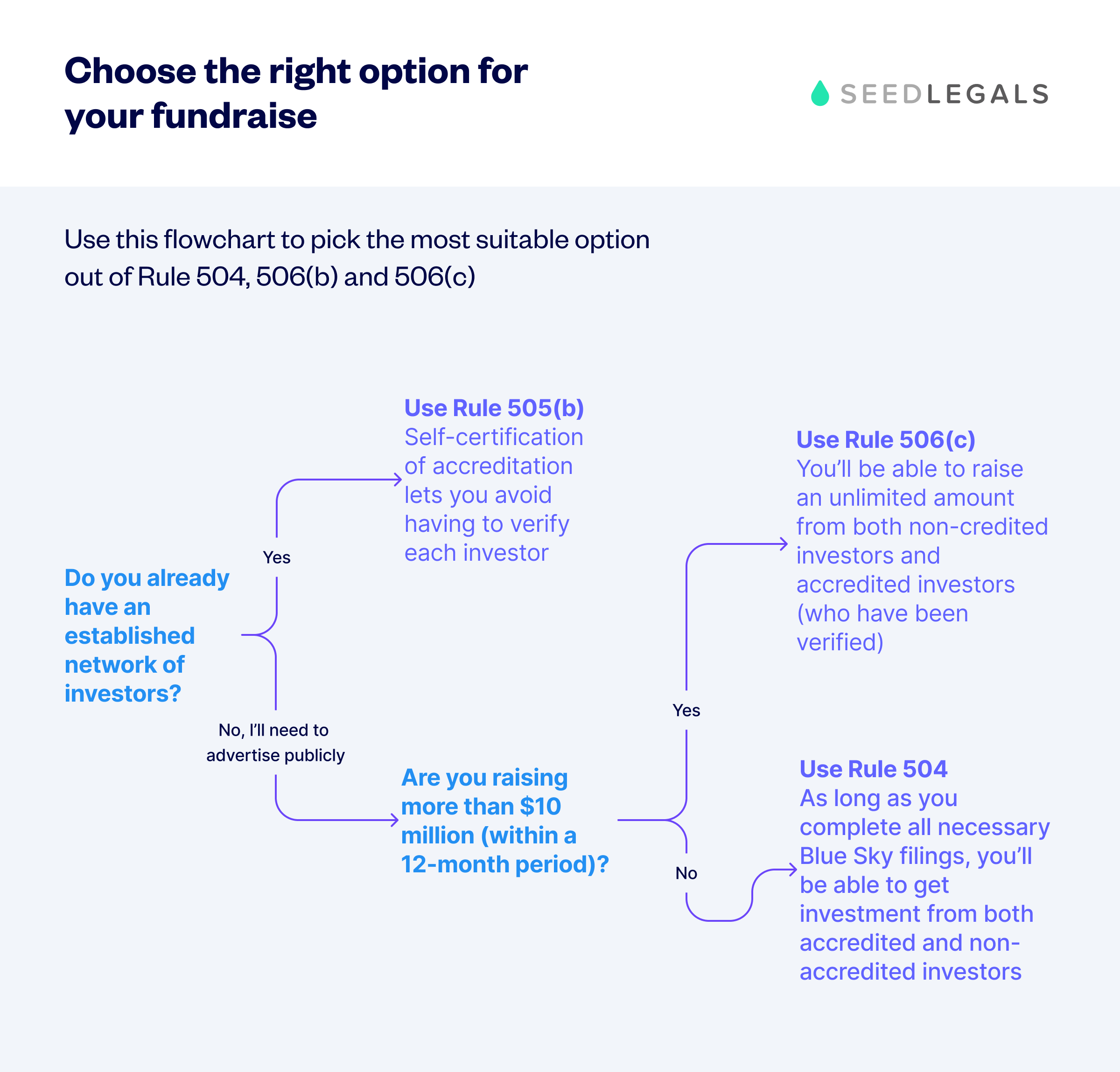

Rule 504 is an exemption you can use if you’re raising up to $10 million within a 12-month period. If you’re a smaller company that wants to raise money without a lot of stringent requirements, it’s often a good choice. This exemption allows “general solicitation” under certain conditions – meaning you can advertise your fundraise publicly.

Under Rule 504, your company would also need to comply with state securities laws (sometimes called “Blue Sky” laws).

Each state will have their own requirements and deadlines, but a lawyer can make sure you’re following the Blue Sky laws that apply. A firm like Lumia can help you with this – they’re experts in identifying and making the right filings for you.

Under Rule 504, you’ll be able to raise money from both “accredited” and “non-accredited” investors.

Rule 506(b) is the exemption that lets you raise money ‘privately’. You can use it to raise an unlimited amount of money without having to register with the SEC.

But you can’t publicly promote your fundraising efforts – as this would count as “general solicitation”. So, if you’re relying on this, you can pretty much only raise money from investors that you have pre-existing relationships with.

Under 506(b), you can raise funds from an unlimited number of self-verified accredited investors. This means they can confirm their accreditation status, and you won’t need to take any extra steps to verify this.

With 506(b) you can also raise money from up to 35 non-accredited investors. But including non-accredited investors makes things much more complicated – they need to be given additional disclosures (like audited financial statements) for their protection.

In reality, most companies fundraising through this route just stick to accredited investors to make things simpler.

Like Rule 504, Rule 506(c) allows startups to publicly promote their fundraise, which can be useful if you don’t already have relationships with experienced investors.

Unlike 504 and 506(b), Rule 506(c) only allows accredited investors to participate. However, the key difference is that under 506(c), the company must take “reasonable steps” to verify that investors are accredited.

This verification process can involve reviewing tax returns, bank statements, or their certifications. In reality, you would outsource this verification process to an external company. The process will mean your fundraise takes longer (you’ll have to gather documents from all your investors) and cost more (you’ll have to pay for the third-party verification company).

The key compliance difference between 504, 506(b) and 506(c) is how investor accreditation is verified. Under 504, you don’t need to conduct any specific investor verification (as you can even accept non-accredited investors under this route). With 506(b), you can rely on investors’ self-certification, but under 506(c), you must take “reasonable steps” to verify their status.

To meet the SEC’s standards, you might need to:

Usually, an external company would handle this verification process for your raise.

The decision between choosing Rule 504, 506(b) or 506(c) depends on your fundraising strategy and resources.

You can use the flowchart below to help you pick the right option for you.

| Rule 504 | Rule 506(b) | Rule 506(c) | |

| Investor limits | Unlimited accredited and non-accredited investors | Up to 35 non-accredited investors (and unlimited accredited investors) | Accredited investors only |

| Limit on amount raised | Up to $10 million within a 12-month period | Unlimited | Unlimited |

| General solicitation to public | Allowed if certain state conditions are met | Not allowed | Allowed |

| Accreditation verification | No specific verification required | Self-certification allowed | “Reasonable steps” required |

| Marketing | Public marketing allowed if state conditions are met | No public marketing | Public marketing allowed |

| Compliance costs | Varied (there are few federal requirements, but number of state law filings depend on specific circumstances) | Lower (no formal verification) | Higher (verification process required) |

If you start your raise as a 506(b) offering (which isn’t public), you have the option to switch to 506(c) and begin publicly advertising.

But, if you begin as a 506(c) offering and share details of your fundraise publicly, you can’t switch back to 506(b).

It’s difficult to switch from either of the 506 options to Rule 504 – this is because the $10 million cap and the state-specific filing requirements make it hard to comply with the rules once you’ve started down another path.

One of the main advantages of Regulation D is that it’s fairly simple to file. Here’s what to know about timing and paperwork:

You can file Form D on your own – it’s not extremely hard. But it’s best to get the help of a lawyer, like Lumia, to make sure you get all the filings right – especially if you have Blue Sky filings to complete too. Getting the submissions wrong could lead to penalties or delays to your fundraising.

Book a free call with our team to find out how we can help with your fundraise.

Want to try SeedLegals for free first? Start your 7-day free trial.

Bring all your questions - we’ve got the answers! We’ll match you with the right specialist.

Starting a company is exciting – but alongside the challenge of building your business comes the task of keeping on top...

PR can be your secret weapon to accelerate deals. Learn how PR can help early-stage startups and founders secure funding...

Learn how the right public relations strategy can open doors, boost recognition and even secure funding, along with comm...