Shares vs. Options: What’s the difference?

The important difference is that if someone owns shares, they are a shareholder immediately. With options, they have own...

Already have an account? Log in

When you sell your company, what happens to the share options that haven’t been allocated to employees? Do they get cancelled? Can the founders allocate the remaining options to themselves? In this article we’ll describe the various scenarios and, importantly, show how founders can allocate unused options to themselves, to undo the dilution they incurred by creating an option pool that was, ultimately, larger than they needed.

Investors usually require the company to create a ‘pre-money’ option pool as part of the first funding round, so that the company is then able to grant share options to its employees.

Why do investors ask for an option pool to be created as part of the first funding round? It’s because creating an option pool dilutes the existing shareholders, and the new investors don’t want to be diluted by the company creating an option pool after their investment. By requiring the company to create a pre-money option pool (which means the option pool is created immediately before the new investments being added), it’s the founders who will be diluted, not the new investors.

That gives the founders a dilemma… what size option pool to create? Make it too small and you’ll need to get shareholder approval to increase it later (awkward, time-consuming). Make it too large and you’ll dilute your own shareholding more than is needed, because when it comes time to sell the company if there are options that have not been allocated to employees, the net effect is the founders diluted themselves unnecessarily.

Founders often ask us about this problem, so we came up with a solution. It’s one of the many advantages of doing your funding round on SeedLegals.

To give share options to your team, your company needs to create an option pool. Our data shows that about half of all companies doing their first funding round create an option pool, and the typical size is 10%, which means the option pool allocation is 10% of the total equity in the company (i.e. 10% of the total numbers of shares, plus the option pool itself).

Shares in the option pool start by being unallocated – that is, you haven’t promised them to anyone yet. As your company grows, you allocate options from the pool by granting share options to team members and advisors.

If, or when you sell your company, you might have already allocated all the options in the option pool. But if there are any remaining, those are the unallocated options. If there are unallocated options, this means the founders created an option pool that was ultimately larger than needed, and therefore they unnecessarily diluted themselves.

There will often be restrictions in the company’s Shareholders Agreements and Articles which say that share options can be allocated to employees, but not to the founders. That’s to avoid founders just giving themselves options whenever they feel like it!

But when it comes to selling the company, if there are unallocated options remaining in the options pool, that doesn’t seem fair because the option pool was created by diluting the founders’ shareholding.

When you do your funding round on SeedLegals, you can add a clause which says that on the sale of the company, unallocated options can go back to the founders:

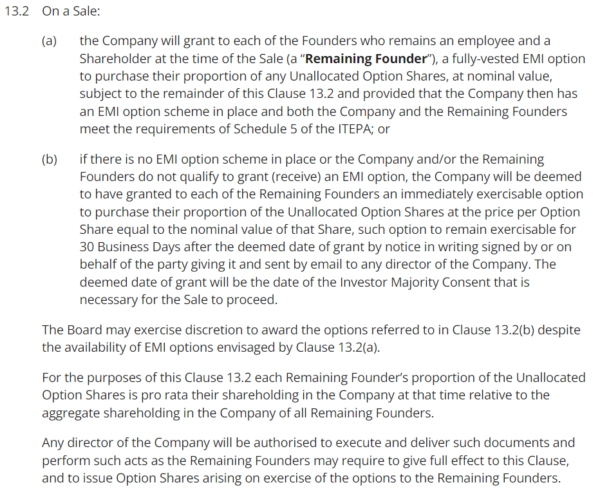

When you’ve enabled this option, this wording will be added to the Sale or IPO section of your Shareholders Agreement:

This wording has your existing shareholders and new investors all agree – and give their approval now, so you don’t have to fight for it later – to allow any unallocated options to be divided between the founders, and for the founders to get them as tax-advantaged EMI options, if the founders and company qualify for EMI at the time.

Note that there can be tax liabilities for the founders when they exercise those options – hopefully a good deal less than the income from the sale of those shares to the acquirer of the company.

When you sell the company it’s the last Shareholders Agreement and Articles that will apply, so if you like this idea, make sure that you enable this option in every funding round. Otherwise, if it’s not enabled in your last round then you won’t have this right.

If you didn’t enable this in your first or previous rounds (or those rounds weren’t on SeedLegals), no problem. You can simply enable these provisions in your next round, and it will take effect from then on.

If you’re reading this and thinking, ‘Oh, I wish I’d known about this before… I’m planning on selling the company… can I still take advantage of this idea?’ – there’s good news. Now you know how this works – and keep reading below for important information on agreeing deal terms with the acquirer – there’s nothing to prevent you going to your shareholders and having them give you these permissions as part of the sales process.

The challenge is that you’ll have to convince your shareholders, which will be more difficult than including this in your deal docs well beforehand.

If you magically chose the perfect size option pool years ago – so all of the options have been allocated by the time you come to sell the company – this makes things easy with the acquirer:

In this scenario there are no unallocated options, and there’s no ambiguity that the acquirer’s cash payment is going to all the shareholders.

But what if there are still unallocated options in the options pool when you sell the company? Then things get trickier – does the purchase price cover the ‘fully diluted cap table’ (which includes any unallocated options), or does it only include allocated options? You’ll need to factor this in when you discuss the sale price with the acquirer or you might be in for an unwelcome surprise.

When the time comes to talk to a potential buyer, you’ll need to carefully check the deal they’re proposing.

Let’s say you’ve agreed a deal with an acquirer that values your company at £100 million.

You have an option pool of 10%, all still unallocated.

Unless you agree otherwise, the default position of the buyer is that they are buying the fully diluted cap table – i.e. their £100 million buys the shares plus the option pool.

But wait… nobody owns those options, so the shareholders don’t get the fraction of the sale price that is allocated to the option pool.

So the shareholders only get £90 million… the acquirer never pays the remaining £10 million, because those options aren’t allocated, so there’s nobody to pay it to. That can be a huge shock if you weren’t aware of this trap.

Whenever you discuss a purchase price with an acquirer, make sure you define whether:

Either way – and especially in the first case above – if the founders have the right to issue any unallocated options to themselves before the sale of the company, that will undo (somewhat…) the dilution they incurred when they created the option pool, and avoid any game playing with the acquirer about deducting the unallocated options from the purchase price.

You might not be thinking about selling anytime soon but you’ll want to add this right to unallocated option into your next funding round. And make sure to preserve that right in each subsequent round because the time you’ll need to call on this will be the last funding round you do before selling the company.

To find out more about setting up an option scheme for your company, book a chat with our experts.

The important difference is that if someone owns shares, they are a shareholder immediately. With options, they have own...

Startups commonly give 1% equity to General Advisors paid only in equity, who work less than 2 days a month. Discover m...

In the UK, 10% is the median amount of equity assigned to EMI share option pools. According to Index Ventures in the US,...